Interest Rates

Read Post

In this post, we are going to touch on what interest rates are, the different types of interest rates one can find in the market and where to source them.

Contents:

Introduction

Interest rate is usually thought of as the cost of borrowing. This is true on the side of a borrower (government, coporation, mortgage etc), but it can also be thought of as the rate one would get when lending (i.e. buying a bond). For most situation, the cost of borrowing definition would suffice. Things get complicated when we get into different currencies and how it affects forward rates as now we have two different countries interest rates to worry about.

Also we need to think about the duration of debt and how interest rates vary across term structures.

US Treasury Rates

The US Treasury borrows money to fund the government spending (especially during fiscal deficit when tax is not enough to fund spending) via issuing Treasury bills, notes and bonds during auction. The secondary market is important here too as the rates that the government can charge depends on existing market rates in the secondary market (price discovery).

Fed Fund Rates

The fed fund rates is the overnight interest rate that banks can borrow in the interbank to meet reserve requirement. In the past, the Fed targets the overnight rate directly via open market operations within a 25bps band set during FOMC meeting. This is what economists call the “Channel System”. The discount rate (the rate at which banks borrow directly from the Fed rather than between themselves) as the upper bound of the band, and there were no lower bound as no interest rate were paid on excess reserves. The weighted average of all the overnight borrowings is known as the effective rate. When the effective rate moved too far from the target rate, the fed will execute open market operations by buying/selling securities to move the rate back to the target rate.

But after the GFC and the implementation of QE, there are too much central bank reserves to implement open market operations efficiently. So the policy changed to have interest paid on excess reserves (IOER - Interest Rate on Excess Reserves), thereby creating a floor system (previously 0% interest rate was paid).

The Fed is able to do a floor system because banks could arbitrage by borrowing at the lower Fed funds rate and lending to the Fed at a higher IOER, thereby causing Fed funds rate to go up.

Due to this new policy change and couple with FDIC’s new capital requirement (Enhanced Supplementary Leverage Ratio (SLR)), an interesting phenomenon has occured in the interbank lending space. Firstly domestic banks have been hesitant to lend while GSEs (Government Sponsored Enterprise) such as Fannie Mae, Freddie Mac and FHLBs (Federal Home Loan) have done most of the lending. This is because GSEs and FHLBs have account with Fed but not eligible to earn IOER (because they do not take in deposits and do not have reserve requirements). This cause Fed Funds rate to go below IOER. As long as they can get some interest, they would be incentivize to lend rather than receiving zero compensation on their EOD cash balances.

Both foreign bank organizations (FBOs) and FHLBs do not take in domestic customer deposits so they not liabile for FDIC insurance fees. Also the new Enhanced SLR regulation cause asset (and hence cash reserve) to be counted into the leverage ratio (so need to increase capital to maintain ratio), making it costly for banks to hold too much cash reserves and they are already awashed with cash after QE so much so that they have to charge large depositors extra fees to deter them from depositing. So only FBOs have the incentive to borrow. Foreign banks will arbitrage the market by borrowing from FHLBs at lower fed funds rate and earn IOER rate. The opportunity cost for lending for FHLBs is zero (anything higher than zero is profitable) and FBOs opportunity cost for borrwing for FBOs is IOER (any rate lower than IOER is profitable).

So in practice, the fed rate was still about 5 to 20bps lower than IOER rate. In September 2013, FOMC introduced the overnight reverse repo agreement (ON-RRP) to allow FHLBs and others to lend to the Fed with collateral at the ON-RRP rate. The ON-RRP rate is set lower than the IOER rate (it is secured borrowings). So now the opportunity cost for FHLBs is no longer 0, but ON-RRP. Hence ON-RRP act as a floor and tend to move the fed funds rate closer to the target rate.

was implemented to make the fed rate higher than IOER. The Fed will post collateral and borrow at the ON-RRP rate. In order to amek this work, the ON-RRP rate has to be lower than the IOER rate.

Because of the possibility of doing a repo, treasury bills are as good as cash.

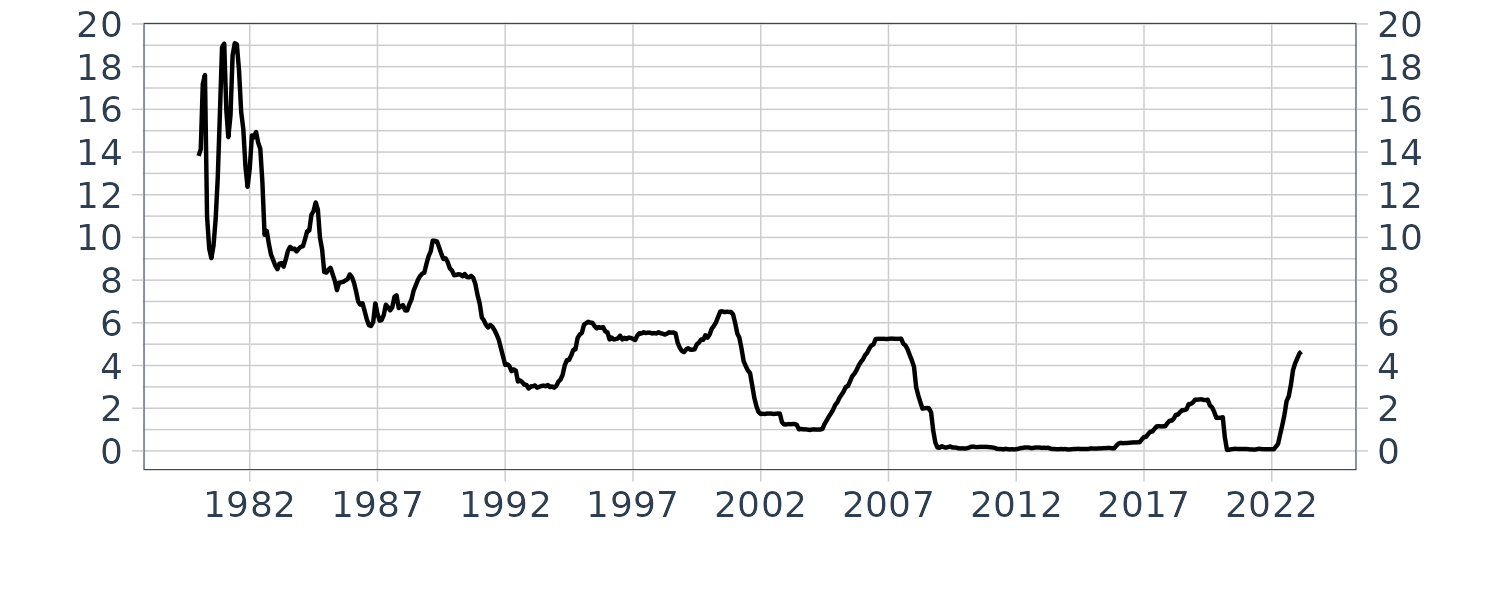

Refer to FRED’s FEDFUNDS ticker for historical data. Let us plot the fed fund rates from 1980 to 2023.

start <- "1980-01-01"

end <- "2023-03-01"

fedfunds <- tq_get("FEDFUNDS", from = start, to = end, get = "economic.data") |>

mutate(

date = yearmonth(date)

) |>

as_tsibble(index = date) |>

fill_gaps()

fedfunds |>

autoplot(price) +

scale_y_continuous(

breaks = seq(0, 100, by = 2),

sec.axis = dup_axis()

) +

xlab("") +

scale_x_yearmonth(date_breaks = "5 year", date_labels = "%y") +

theme_tq()

The 30-Day Fed Funds futures can be traded via the ticker “ZQ”. For example, the futures “ZQU3” (expiring SEP 2023) is showing a price of $94.995. This implies an average daily rate of \(100 - 95.995 = 4.005%\) of interest in September. Using Futures prices (based on market expectations) from CME, it is possible to calculate the probability of the Fed hiking or cutting interest as shown here Fed Rate Monitor Tool.

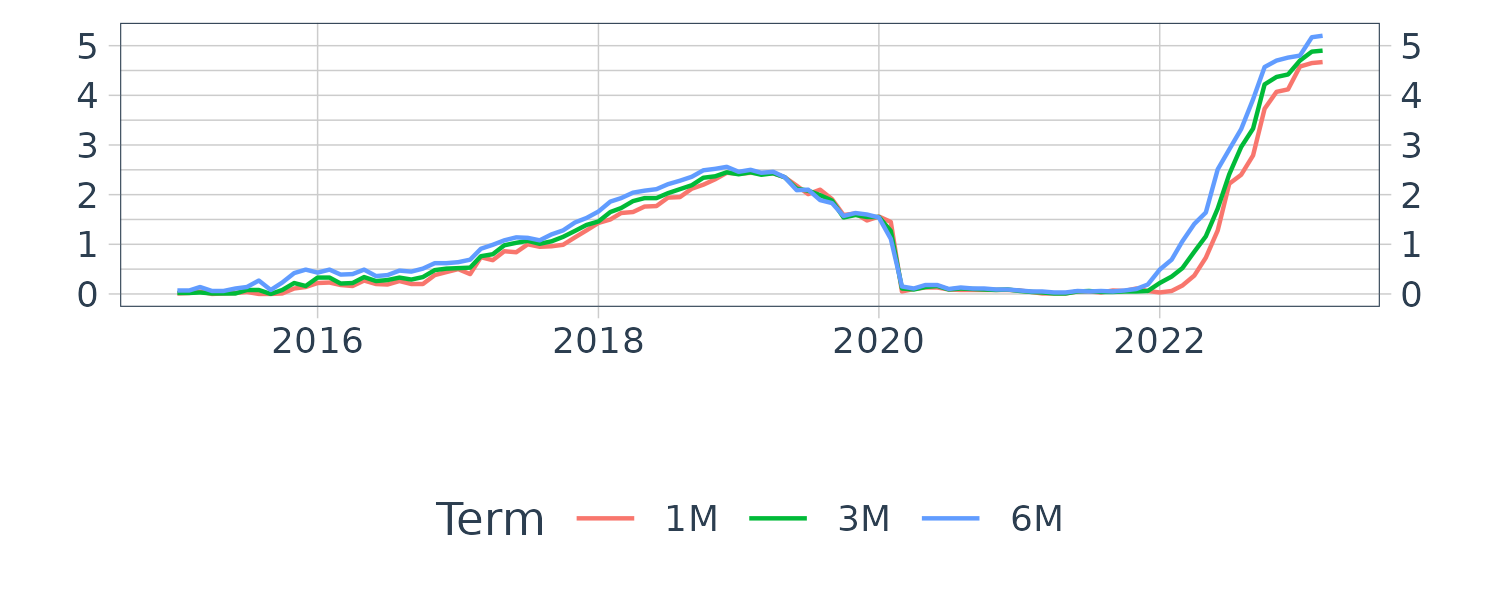

Treasury Bills (Money Market)

Money market comprise of short term debt that ranges from overnight to less than a year. They are sold at a discount to par value, pay no coupons, and mature at par.

Commerical banks often fund/borrow short term from the money markets and buy/lend longer-tenor less liquid assets. There are both secured and unsecured money markets.

Repo and FX Swaps are two examples of secured money markets. Repo can be used to purchase Treasuries on leverage. The amount the investor needs to put down would be the haircut that would be deducted from the full value. FX swap is considered secured as well because the notional in the other currency is exchanged as collateral.

Examples of unsecured money markets are Certificate of Deposit (CDs), commerical papers (CP), Fed Fund and treasury bills.

Here are a list of available on FRED:

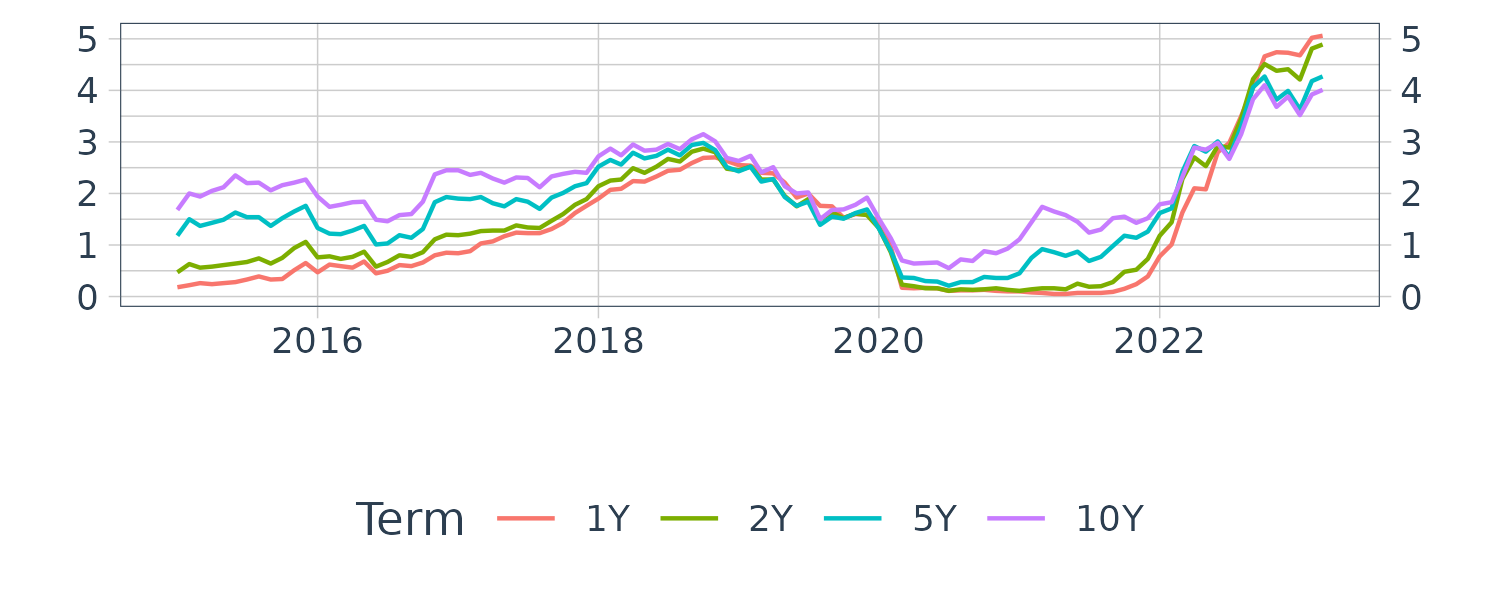

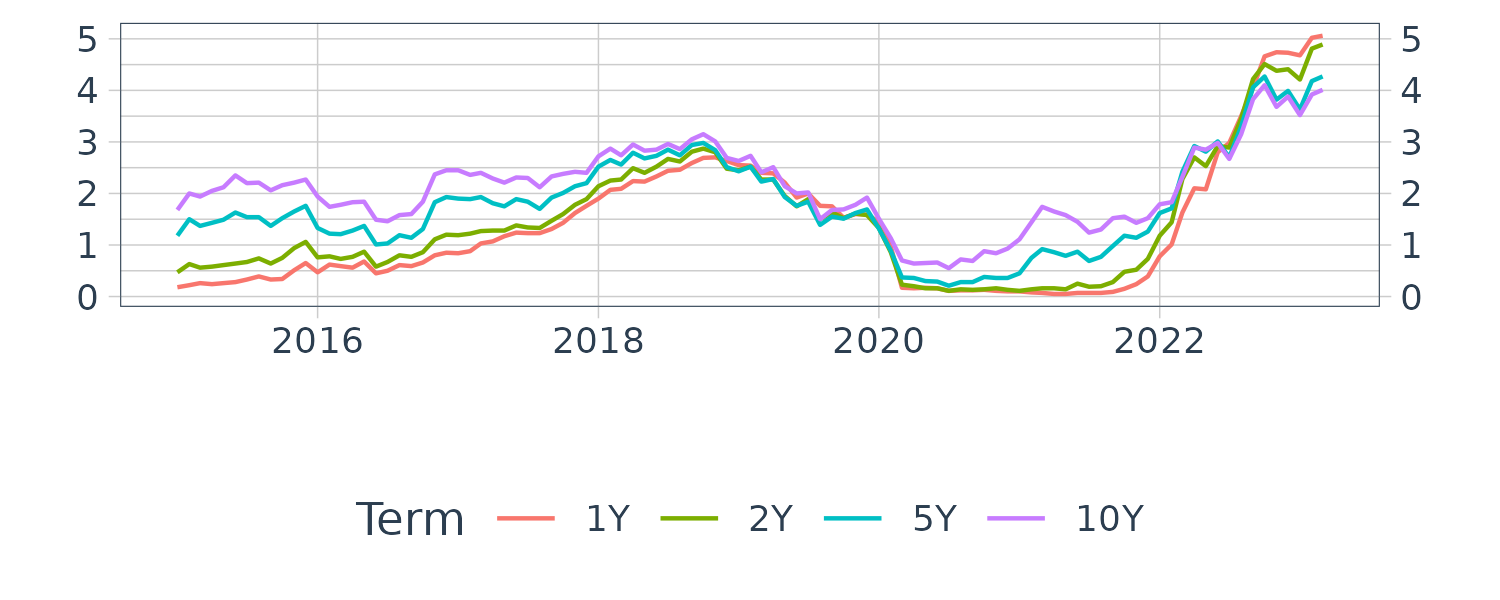

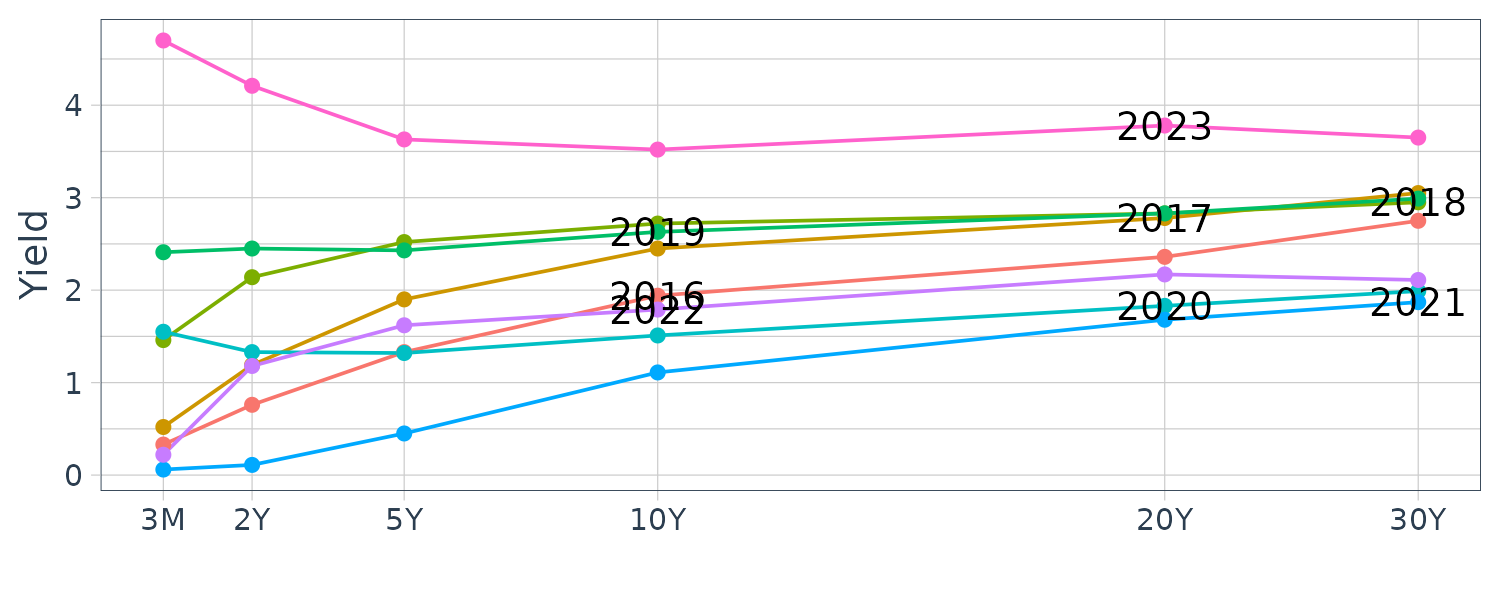

We can see on the graph that the longer dated yields tend to lead shorter dated ones which shows longer dated yields do predict shorter dated yields consistently. Also longer dated yields tend to be higher than shorter dated ones except when the yield curve inverts.

And also EuroDollars Futures:

Money Market Reform 2016

SEC announced in 2014 (to be implemented in 2016), the ability for Prime MMF to freeze redemptions in times of market stress. This in turn cause a mass exodus of funds from Prime MMF to Govt MMF as institutional investor fear their funds might be freezed in times of need. Foreign banks are mostly the side that is borrowing money in Prime MMF and this cause foreign banks to turn to secured borrowings rather than unsecured borrowings in MMF.

Treasury Notes

Treasury notes comprise of medium term debt that ranges from 1y to 10y and pay coupons every 6 months. Here are a list available on FRED:

Treasury Bonds

Treasury notes comprise of long term debt that ranges from 20 years onward, and also pay coupons every 6 months.. Here are a list available on FRED:

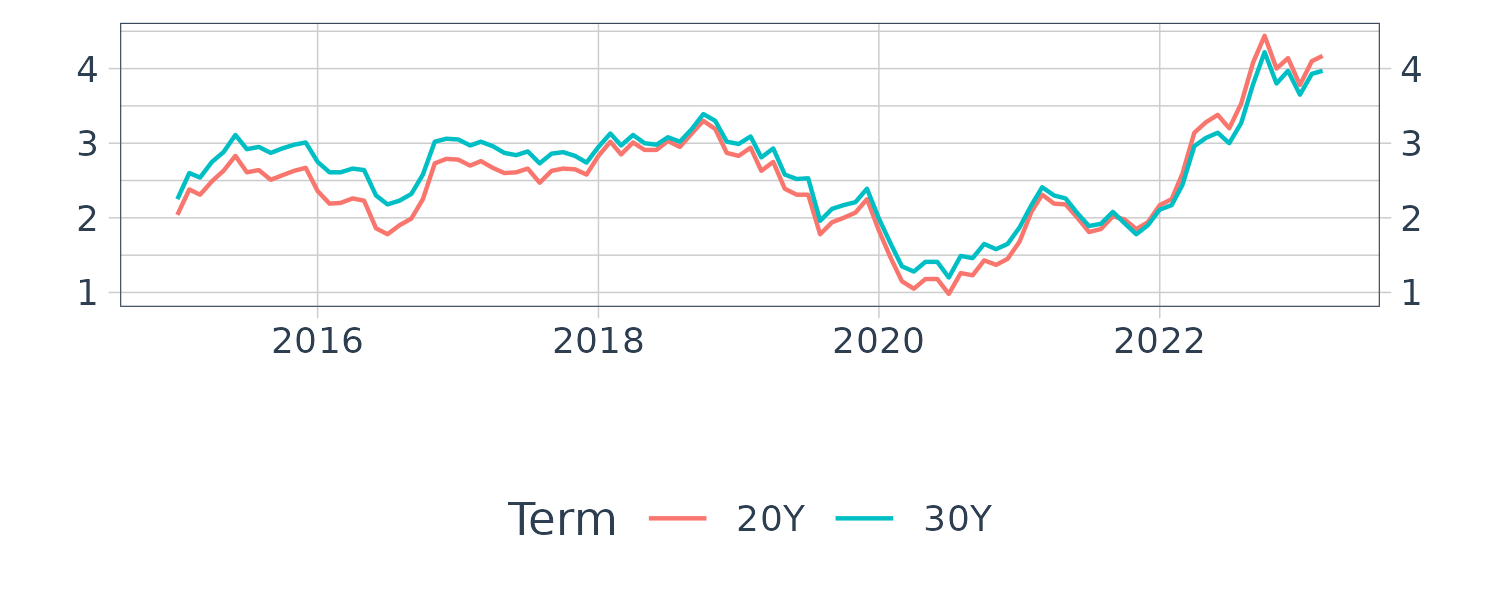

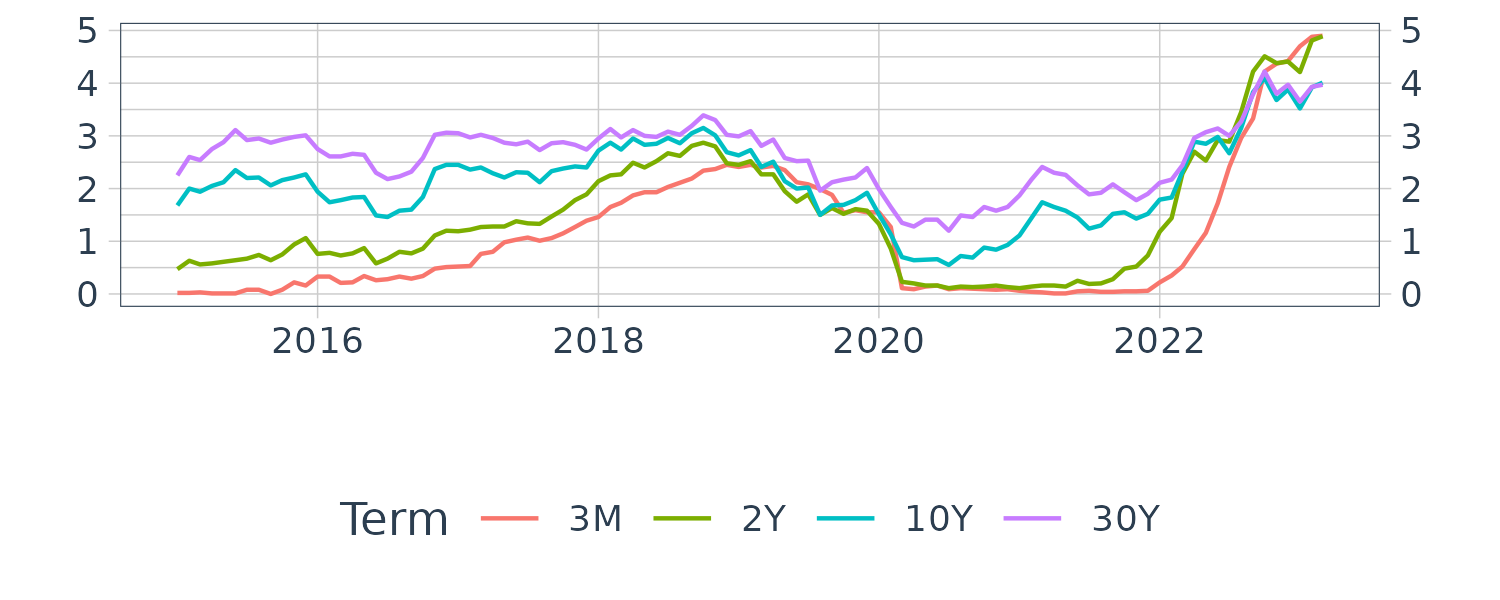

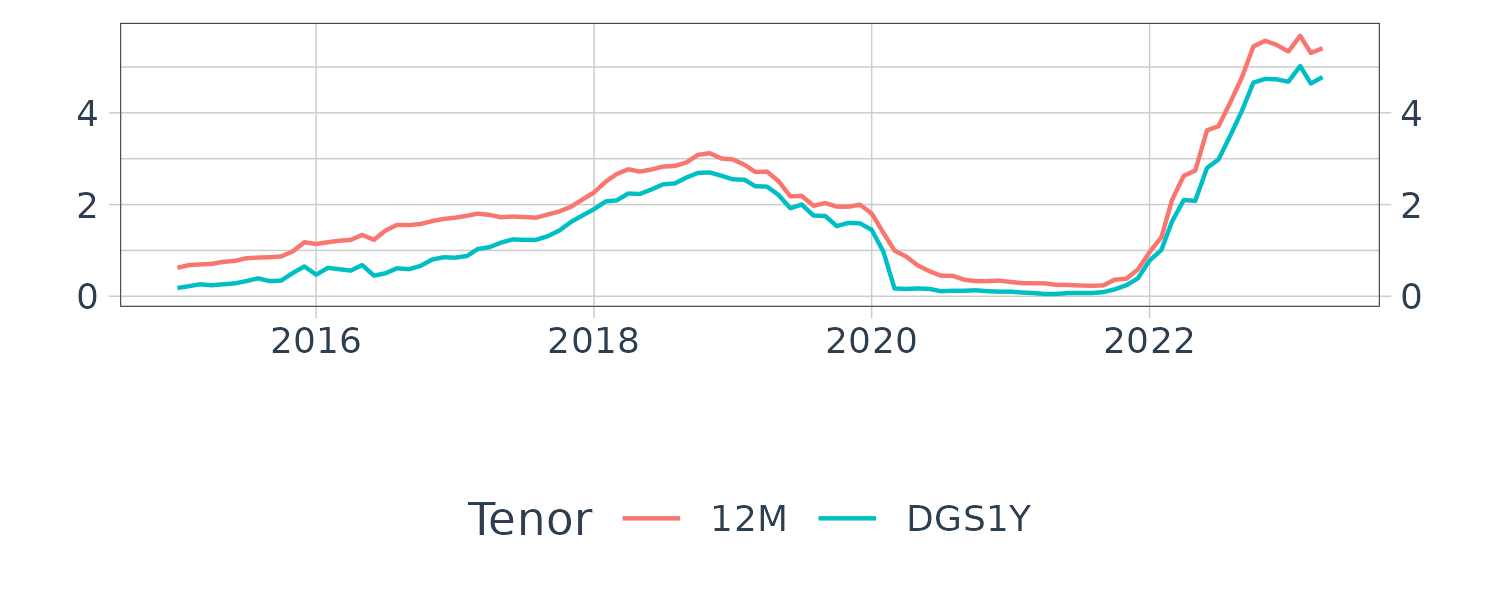

Let us graph a few popular tenures across short to long term duration:

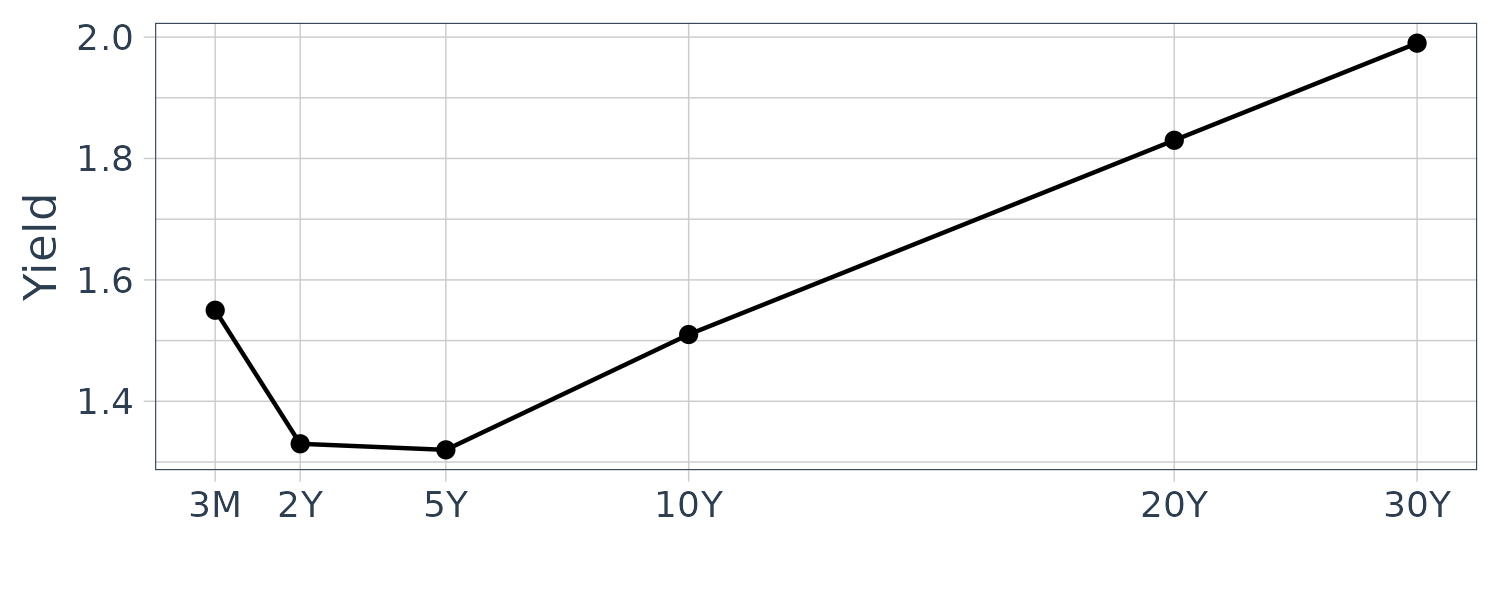

Another way to look at yields across tenures is the yield curve. It shows the cross sectional yields at a point in time. For example, this is the yield curve at the begining of 2020:

And across time from 2016:

Interbank Rates (LIBOR)

The London Interbank Offered Rate (LIBOR), was established by the British Bankers’ Association (BBA) but now being administered by ICE (Intercontinental Exchange) and published by Reuters. LIBOR is slowly being phased out in favor of risk free rates.

The LIBOR fixings are calculated based on borrowing cost estimates submitted by major international banks in the UK and is open to manipulation. The following question is asked of to the member banks: “At what rate could you borrow funds, were you to do so by asking for and then accepting interbank offers in a reasonable market size just prior to 11 am?” The average based on trimmed mean is then calculated and published.

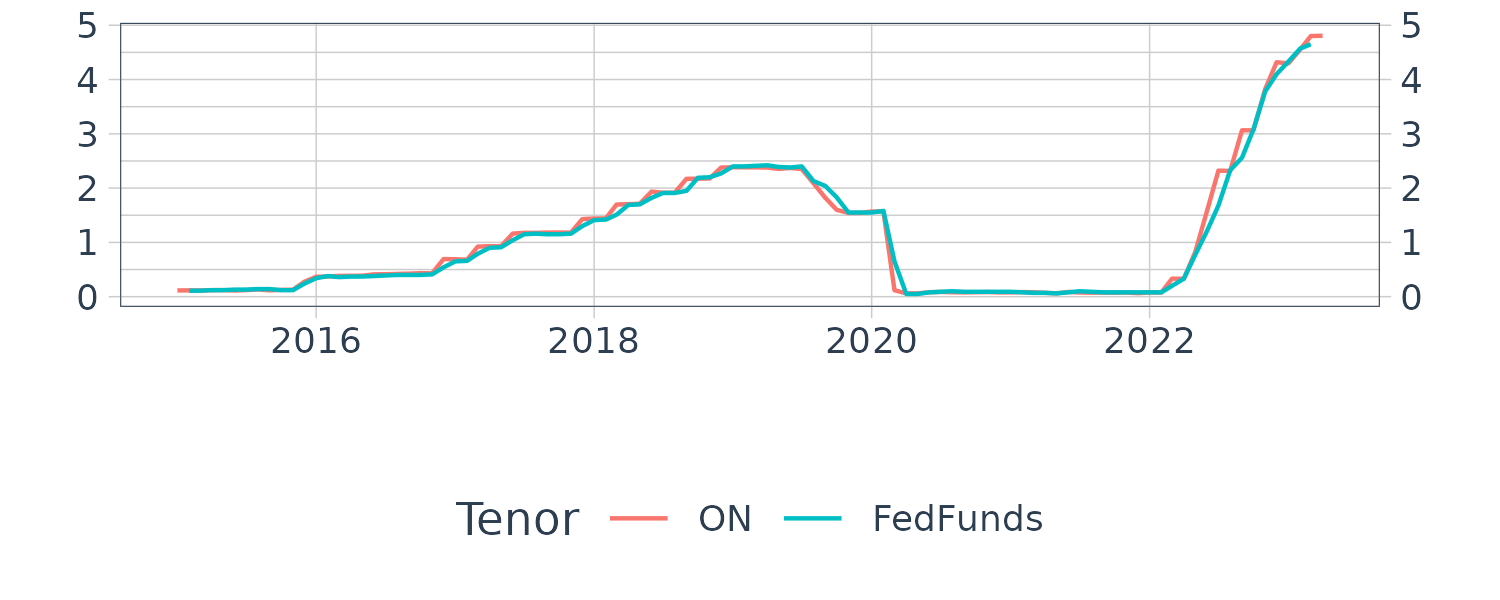

The key difference between LIBOR and the Fed fund rates is the geography. Fed fund is influenced by the Fed and are based on funds housed in the US while LIBOR is based on Eurodollar deposits funds housed outside of the US. They are often in lockstep with each other but can sometimes diverge.

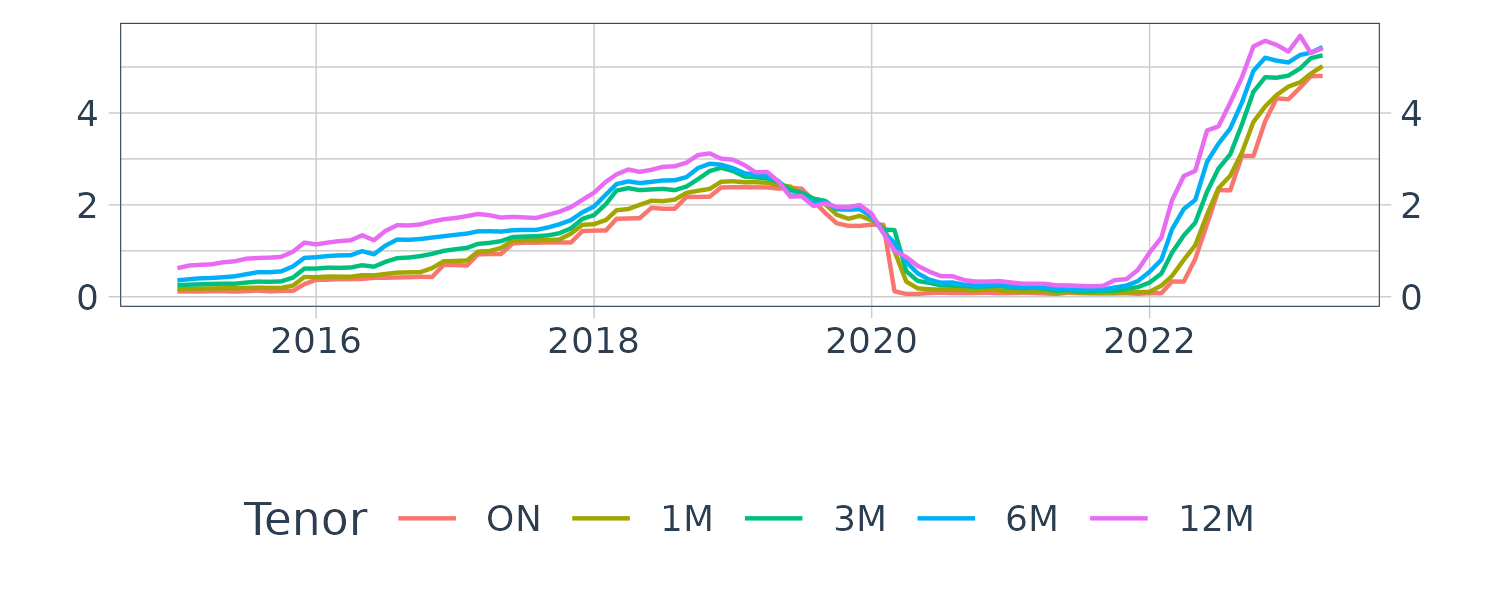

LIBOR is published for multiple currencies but we will only focus on USD here. The LIBOR data is sourced from iborate.com

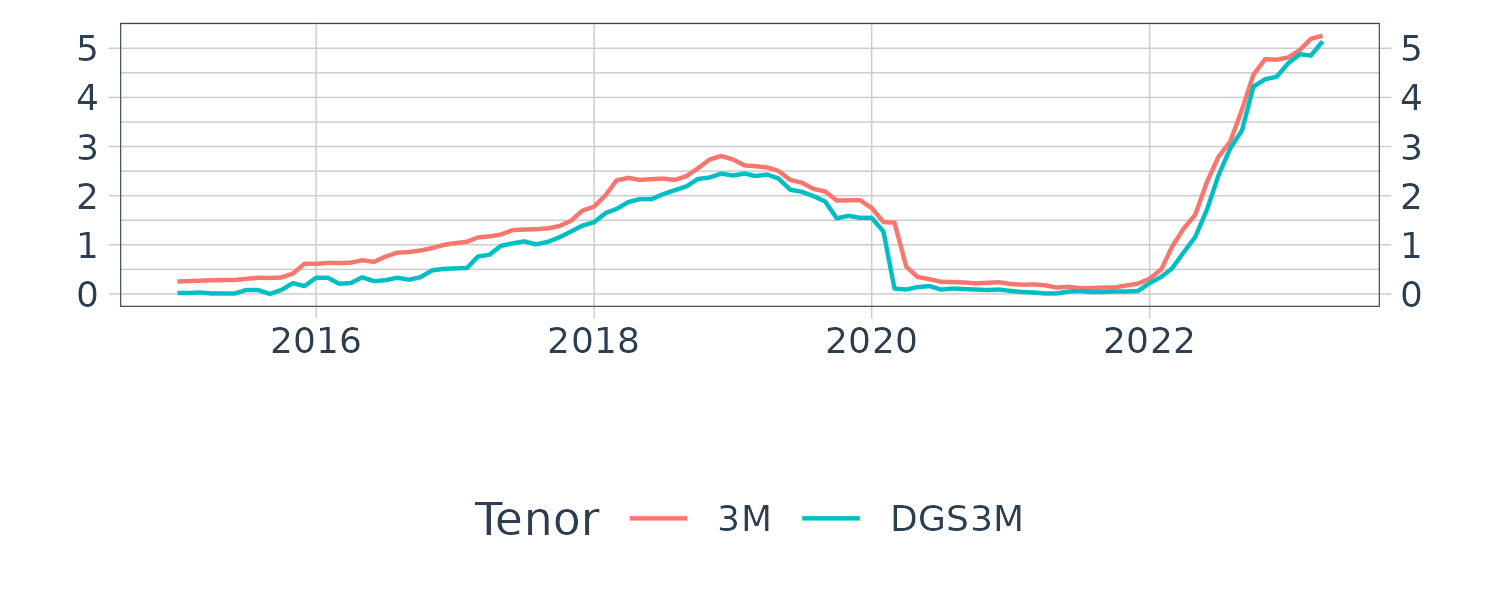

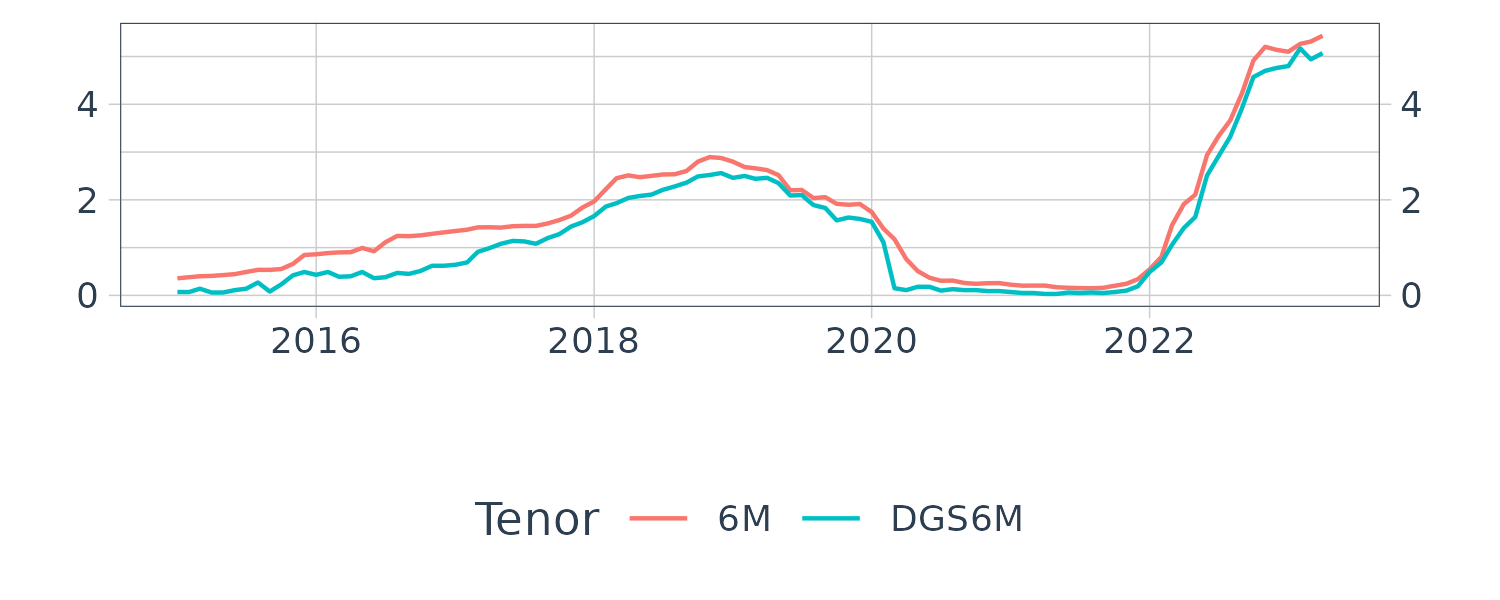

How about the difference between LIBOR and Treasury rates? Treasury rates are prefix with DGS:

We can clearly see a credit spread between LIBOR and Treasury rates.

Repo Rates

Both the Treasury and LIBOR rates are unsecured borrowings. Repo rates are what we call secured borrowings. Treasury securities are sold and bought back (usually ON but could be term). The difference in the price is the interest charged and is the repo rate.

As the securities is pledged usually with a central counterparty, there is very little credit risk involved and the repo rate is lower than corresponding Treasury rates.

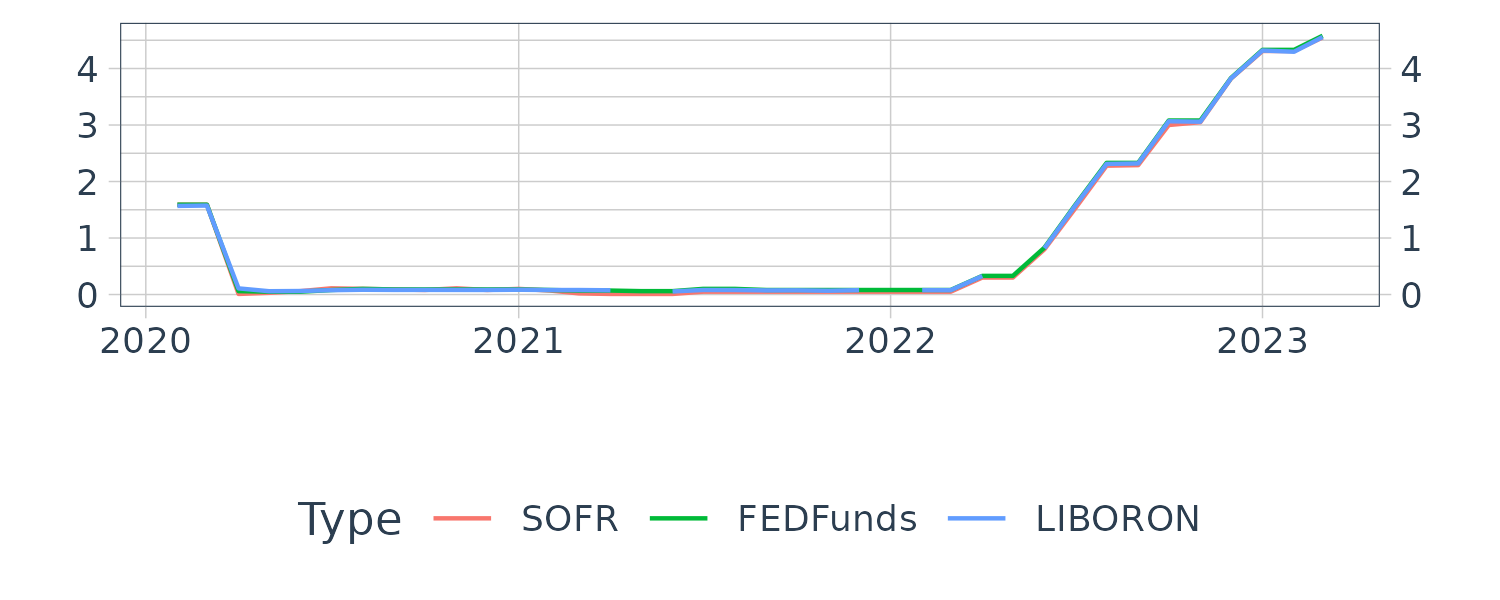

The Secured Overnight Financing Rate (SOFR) is a volume-weighted median of the actual ON rates transacted in the US. Do not confused this secured borrowings rate with other countries ON rates (such as Sterling SONIA, Euro ESTER, Swiss SARON, and Japan TONAR) that are unsecured rates and more similar to the Fed Funds rate.

SOFR fixings is published the next business day at 08:00 am EST.

As discussed in the Fed Funds section, the fed funds market has lost its importance as commerical banks do not borrow or lend in the market post GFC and so do not reflect actual funding conditions. This makes SOFR even more important as it is more representative of the true funding market conditions.

SOFR can be sourced from FRED.

For tenors longer than ON, the SOFR rate is calculated based on compounding SOFR rates based in the past. Hence SOFR rate is backward looking rather than Treasury or LIBOR forward looking rates.

References

Interest Rate Control Is More Complicated Than You Thought

The Federal Funds Market since the Financial Crisis

How Did the Fed Funds Market Change When Excess Reserves Were Abundant?