Fed Balance Sheet

Read Post

In this post, we will go through the factors affecting central reserves balances as shown in H.4.1 Factors Affecting Reserve Balances

Contents:

Introduction

The dual mandate of the Fed is to promote maximum sustainable employment, and price stability. The Fed’s balance sheet helps to achieve these goals. When Fed increase its holdings of debt instruments (Treasury securities and MBS) (expanding the balance sheet), it is seeking to loosen financial conditions by increasing the price of the debt instruments and lowering the yield. The Fed pays for this by creating bank reserves. Likewise, decreasing its holding of such instruments (contracting the balance sheet) would lower the price and increase the yields, thereby constraining financial conditions and asset prices. Bank reserves are extinguish in this case.

Each week, the Fed publishes the balance sheet on Thursday around 4:30pm EST. The balance sheet can be found on Table 5 here.

Central Bank Reserves

The Fed can buy financial assets or create loans by creating bank reserves (IOU) as liabilities to pay for them. These reserves are used by commerical banks with accounts with the Fed to settle payments with one another. For example, commerical banks can use bank reserves in their fed account to pay another bank if a customer transfer from one commerical bank to the other.

The Fed used to conduct open market operations by tweaking the level of such reserves (open market operations) by buying and selling Treasury securities. But after 2008 GFC led quantitative easing program, the Fed has balloned its reserves to trillions of dollars. Now, Fed controls short term interest by adjusting the interest it pays on excess reserves and when commerical bank loan money to the Fed via the Overnight Reverse Repo Facility.

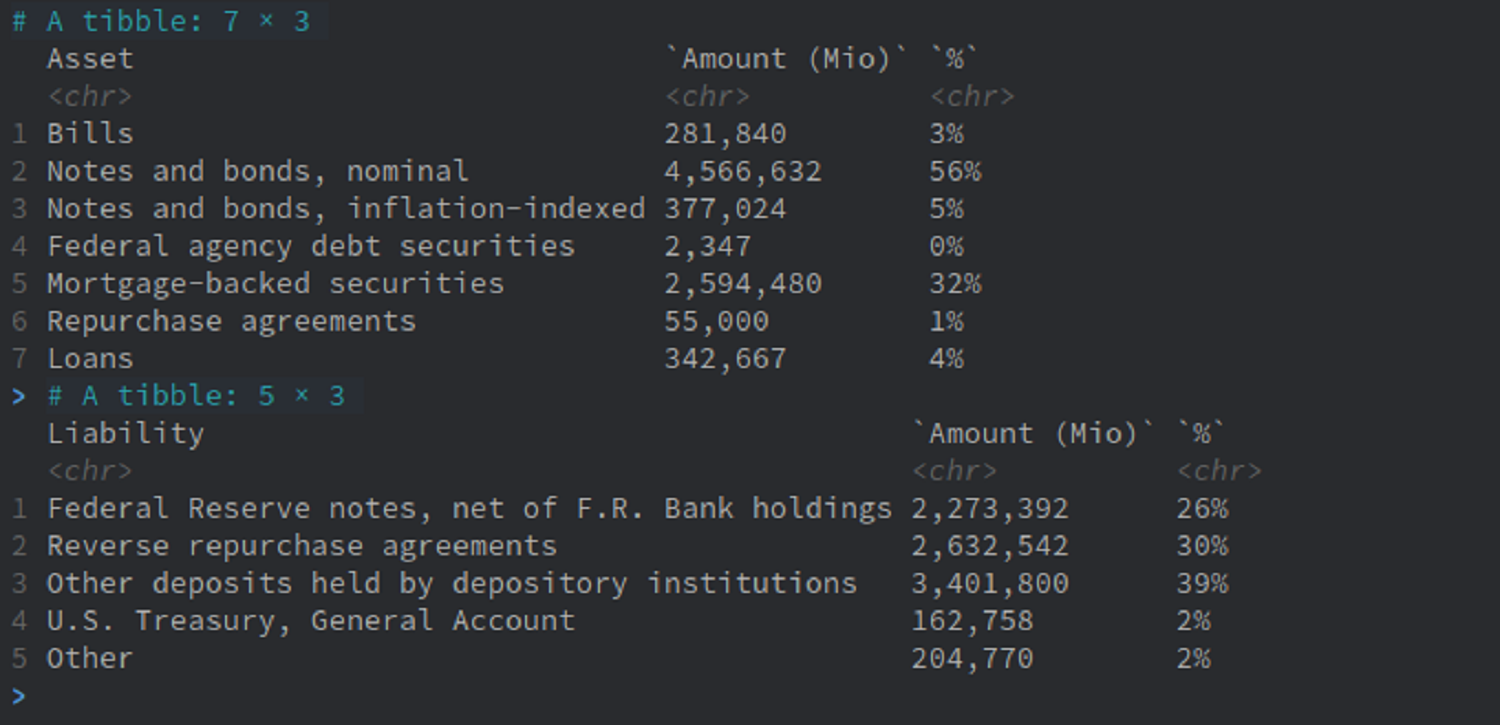

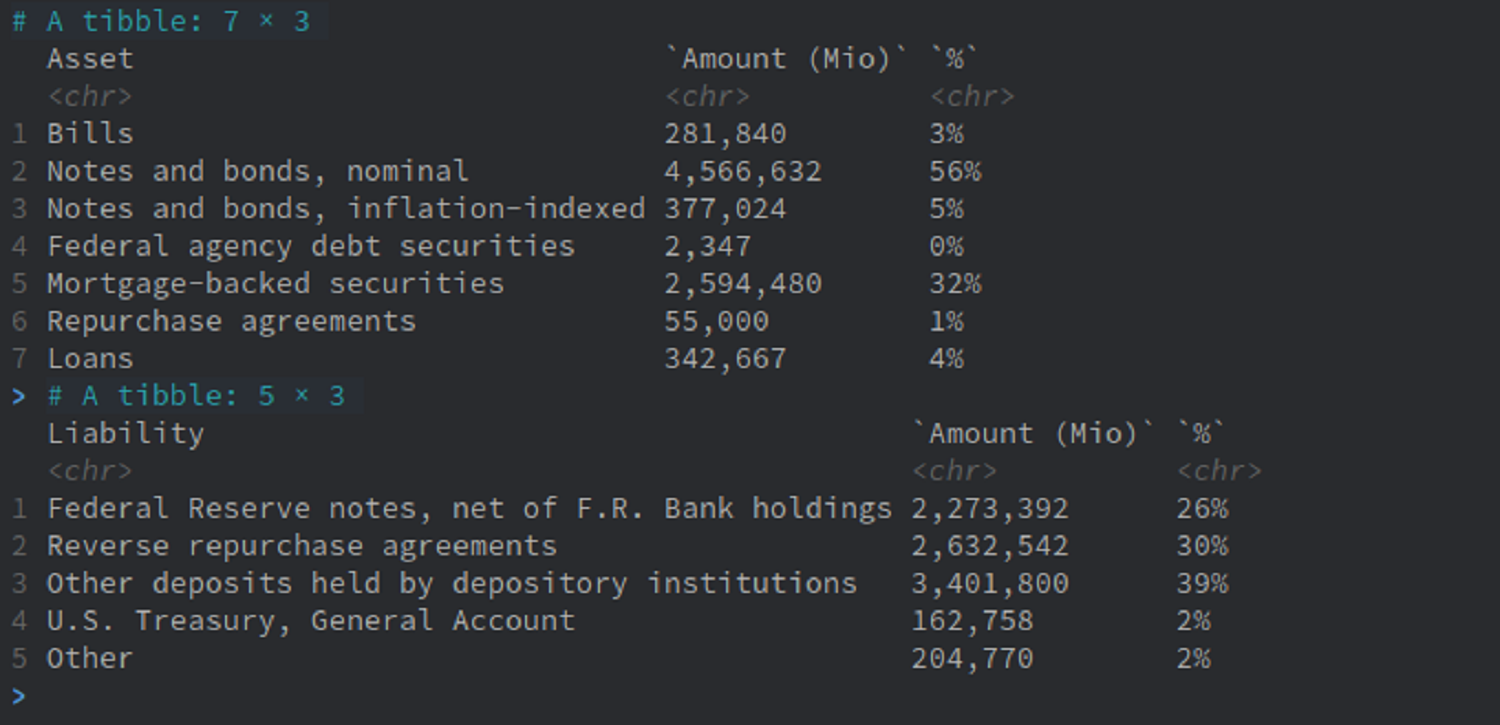

Fed Assets

We will be using data released on Mar 29th 2023 for analysis.

Securities Held Outright

The debt instruments that Fed holds are US Treasury securities such as:

- Bills

- Nominal Notes and Bonds

- Inflation-Indexed Notes and Bonds (TIPS)

And other debt securities:

- Federal Agency Debt Securities

- MBS

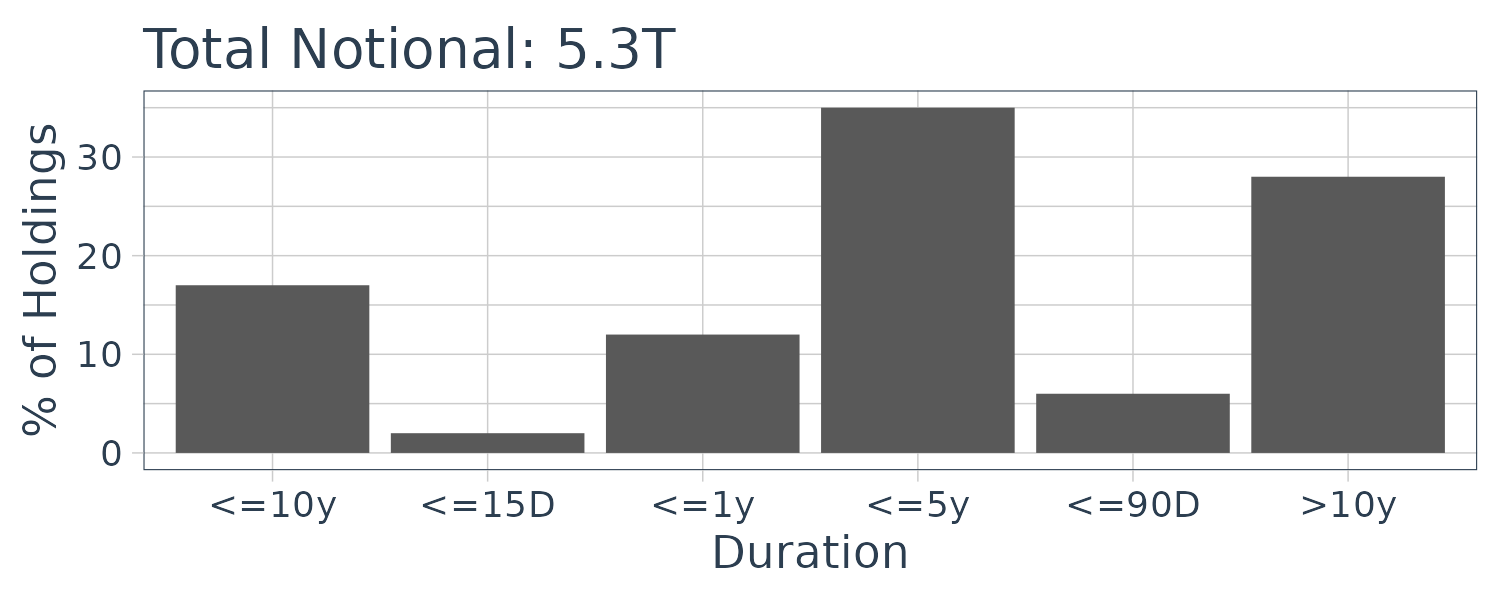

We can see the duration distribution for Treasury securities with a total notional of 5.3T:

Due to QT, Treasury notes/bonds are not rolled over when the mature. The roll-off is capped at $60 bio per month. The inflation component of TIPS is not paid in cash but added to the principle, causing the roll-off to be less than $60 bio per month. The cap is reserved for Treasury coupon bonds, and if there is any room left, will be used for Treasury bills. Hence, bills have lower priority for rolling off compared to coupon bonds. For MBS, they are rolled-off by prepayments, refinanced, and regular mortgage payments. The monthly cap is $35 bio per month.

As you can see, due to past QE, the Fed has accumulated big portion of longer dated bonds but the number is decreasing as the Fed is currently on QT.

Federal Agency debt securities are insignificant as it has a notional of 2.3 bio and not even 0.1% of Treasury securities.

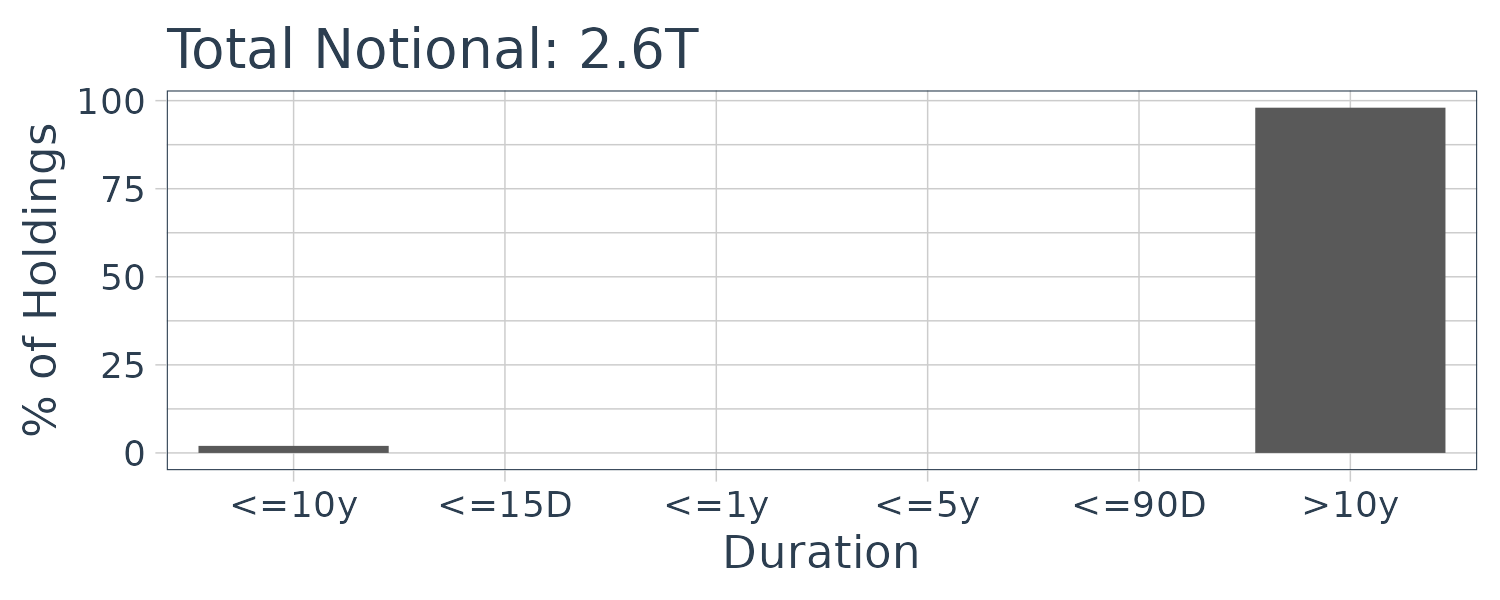

The duration distribution for MBS with a total notional of 2.5T:

Repurchase Agreements

Repo transactions are a way for commerical banks to borrow reserves via a structured loan to the Fed and a tool for the Fed to control ON interest rate.

Standing Repo Facility (SRF)

The Standing Repo Facility (SRF) is established in 2021 to act as a ceiling to reduce the upward pressure of overnight interest rate. If ON rate increase above the Interest on Reserve Balances (IORB) set by the Fed, the Fed will engage in REPO transaction to lend out at rates below IORB. The FOMC sets the SRF minimum bid rate, and the actual SRF rate is discovered via auction. Thus, this is no reason for counterparties with access to the SRF to borrow above the SRF rate.

The facility counterparties are mostly primary dealers and commerical banks.

Repo are short term in nature and has duration under 15 days and notional of about 60 bio.

Foreign and International Monetary Authorities (FIMA) Repo Facility

Repo facility for foreign central banks. The role is the same as SRF as described above but for foreign central banks. This allows the foreign entities to temporarily exchange their Treasury securities in exchange for USD, which can be used outside the Federal system.

An example is the Swiss National Bank (SNB) using the facility to provide dollar liquidity to UBS for the takeover of Credit Suisse.

Loans

Commerical banks have access to 3 types of discount window credit. They are Parimary, Secondary, and Seasonal credit. Each has their own “discount rate”.

Loans under discount window lending amount to approximately 342 bio.

Primary Credit

Primary credit lending program is primarily for sound depository institutions and no restrictions on the use of funds. The rate is priced relative to the target range of the fed funds rate. Collaterals are posted at fair market value.

During the SVB crisis, there was a spike in the borrrowing in the Primary Credit program.

Secondary Credit

Secondary credit is a lending program for depository institutions that do not qualify for primary credit. The interest rates are higher than primary rates with restrictions (such as restricting the expansion of assets). Also higher haircuts are applied to the collaterals pledged.

Seasonal Credit

Seasonal credit is a lending program for small depository institutions (with deposits of $500 mio and below) with seasonal liquidity problems.

Other loans outside of Fed discount window:

Paycheck Protection Program Liquidity Facility (PPPLF)

The facility assists the Small Business Administration’s Paycheck Protection Program (PPP) by providing liquidity to banks administering these PPP loans to small busineses to help them pay their workers payroll.

Bank Term Funding Program (BTFP)

Make additional funding available to banks who have small businesses and household as depositors. In time of crisis, the BTFP is able to hold high-quality sercurities as collateral so that the institution does not need to fire sale them in times of need.

During the SVB crisis, banks can borrow at a fixed rate pegged to the 1Y ON index swap rate plus 10bps for up to a year. Banks can post collateral that are valued at par. Some banks borrow from BTFP to return the more costly primary credit in the discount window.

Other Credit Extensions

Secured loans that allow business to extend credit to their customers. Includes loans that were exteneded to banks that were subsequently placed into FDIC receivership. These loans are secured by collateral.

Fed Liabilities

Currency in Circulation

There are about 2.3T USD fiat (paper) currency in circulation around the world. A vast majority of fiat currency are offshore and a significant number have links to criminal offence. When commerical banks needs fiat currency, it will exchange central bank reserves for currency (sent by armour trucks from Fed), and this is one way central bank reserves can be leave the Fed balance sheet.

Reverse Repurchase Agreements

Reverse repo are borrowings of Treasury securities from commerical banks and the Fed uses this to maintain the Fed Funds rate.

Reserve Balances with Federal Reserve Banks

Is the amount of money that commerical banks maintain in their accounts with the Fed and constitutes the largest component of the liabilities (3.4T). This is the same as what is described in the Central Bank Reserves section.

Deposits with F.R. Banks, other than reserve balances

U.S. Treasury General Account (TGA)

When payments are made to the US Treasury, such as tax payments, it is credited into the TGA and payments such as Social Security checks and interest on federal debt. It is essentially a checking account for the US Treasury. It contains about 183 bio.

Others

These include deposits under GSEs such as Fannie Mae, and Designated Financial Market Utilities (FMUs) such as the CME clearing house and CLS. Financial market utilities (FMUs) are systems that provide the infrastructure for transferring, clearing, settling payments, etc.

Scrap Data

It is possible to download the Fed Balance sheet tables in csv, but for our purpose, let us try to scrap the data that is described in this post instead:

library(rvest)

url <- "https://www.federalreserve.gov/releases/h41/20230330/"

page <- read_html(

paste0(url)

)

assets <- c(

"Bills",

"Notes and bonds",

"Federal agency",

"Mortgage",

"Repurchase",

"Loans"

)

liabilities <- c(

"Federal Reserve notes",

"Reverse repurchase",

"General Account",

"Other13",

"Other deposits"

)

asset_data <- page |>

html_nodes("div:nth-child(17)") |>

html_table() |>

nth(1) |>

select(X1, X3) |>

mutate(

Amt = as.numeric(gsub(",", "", X3))

) |>

rename(

Asset = X1,

`Amount (Mio)` = X3

) |>

filter(str_detect(Asset, paste0(assets, collapse = "|"))) |>

mutate(

Asset = gsub("[[:digit:]]+", "", Asset)

)

total <- sum(asset_data$Amt)

asset_data <- asset_data |>

mutate(

`%` = paste0(round(Amt / total * 100), "%")

) |>

select(-Amt)

liability_data <- page |>

html_nodes("div:nth-child(19)") |>

html_table() |>

nth(1) |>

select(X1, X3) |>

mutate(

Amt = as.numeric(gsub(",", "", X3))

) |>

rename(

Liability = X1,

`Amount (Mio)` = X3

) |>

filter(str_detect(Liability, paste0(liabilities, collapse = "|"))) |>

mutate(

Liability = gsub("[[:digit:]]+", "", Liability)

)

total <- sum(liability_data$Amt)

liability_data <- liability_data |>

mutate(

`%` = paste0(round(Amt / total * 100), "%")

) |>

select(-Amt)

See Also

References

H.4.1 Factors Affecting Reserve Balances

Credit and Liquidity Programs and the Balance Sheet

Understanding the Federal Reserve Balance Sheet

The structure of Federal Reserve liabilities

Standing Repurchase Agreemnt (repo) Facility

Foreign and International Monetary Authorities (FIMA) Repo Facility

Paycheck Protection Program Liquidity Facility