Bookkeeping

Read Post

In this post we will follow the tutorials from the YouTube channel “Accounting Stuff” using GNUCash.

Contents:

The Accounting Cycle

- Identify Transactions

- Prepare Journal Entries

- Post to General Ledger

- Unadjusted Trial Balance

- Post Adjusting Entries

- Adjusted Trial Balance

- Create Financial Statements

- Post Closing Entries

The Accounting Equation

\[\begin{aligned} \text{Stuff the Business Owns} &= \text{Stuff the Business Owes}\\ \text{Assets} &= \text{Liabilities} + \text{Equity} \end{aligned}\]Expanded Accounting Equation

\[\begin{aligned} \text{Assets} &= \text{Liabilities} + \text{Equity}\\ \text{Equity} &= \text{Capital Contributions} + \text{Retained Earnings}\\ \text{Retained Earnings} &= \text{Accumulated Profits} - \text{Withdrawals}\\ \text{Accumulated Profits} &= \text{Revenue} - \text{Expenses} \end{aligned}\]Debits and Credits

“Economic Benefit” is the potential for an asset to contribute either directly or indirectly to the flow of an entity’s cash. For every transaction, there involve a flow of economic benefit from one account to the other.

Debits represent the flow of economic benefit to a destination, while credits represent the flow of economic benefit from a source.

Debits:

- Assets

- Expenses

- Dividends

Credits:

- Owner’s Equity

- Liabilities

- Revenue

The source of funds come from Credits accounts such as Owner’s Equity, Liabilities (borrowings) and Revenue (income from business). These source of funds are then channelled to Assets, Expenses and Dividends.

As seen above, Assets are represented as Debits and Liabilities as Credits. How about Equity? We know that Owner’s Equity can be broken up into:

\[\begin{aligned} \text{Equity} &= \text{Owner's Equity} - \text{Dividends} + \text{Retained Earnings}\\ \text{Retained Earnings} &= \text{Revenue} - \text{Expenses}\\ \text{Equity} &= \text{Owner's Equity} - \text{Dividends} + \text{Revenue} - \text{Expenses} \end{aligned}\]Using the Accounting Equation:

\[\begin{aligned} \text{Assets} &= \text{Liabilities} + \text{Owner's Equity} - \text{Dividends} + \text{Revenue} - \text{Expenses} \end{aligned}\] \[\begin{aligned} \text{Dividends} + \text{Expenses} + \text{Assets} &= \text{Liabilities} + \text{Owner's Equity} + \text{Revenue} \end{aligned}\]We moved all the negative accounts to the LHS to make them positive. So now the LHS represents Debits and RHS represent Credits. Debits increase when debited and Credits increase when credited. Hence, Debits decrease when credited, and Credits decrease when debited for the equation to balance.

The confusion people get is because it seems that in our everyday language, we reverse the concept of debit and credit. This is because we view debit/credit from our point of view. From a bank customer point of view, a checking account is an asset but from a bank’s point of view, a checking account is a liability. So debit/credit reverse.

The acronym “DEALER” can help to remember which is on the LHS and RHS.

\[\begin{aligned} \text{D} &= \text{Dividends}\\ \text{E} &= \text{Expenses}\\ \text{A} &= \text{Assets}\\ \text{L} &= \text{Liabilities}\\ \text{E} &= \text{Equity}\\ \text{R} &= \text{Revenue} \end{aligned}\]Dividends, Expenses and Assets are “Debits” accounts. Economic benefit flows to them. They increase when debited and decrease when credited.

Liabilities, Equity, and Revenue are “Credits” accounts. Economic benefit flow from them. They decrease when debited and increase when credited.

T Accounts

In a T account representation, debits always go on the left and credits on the right.

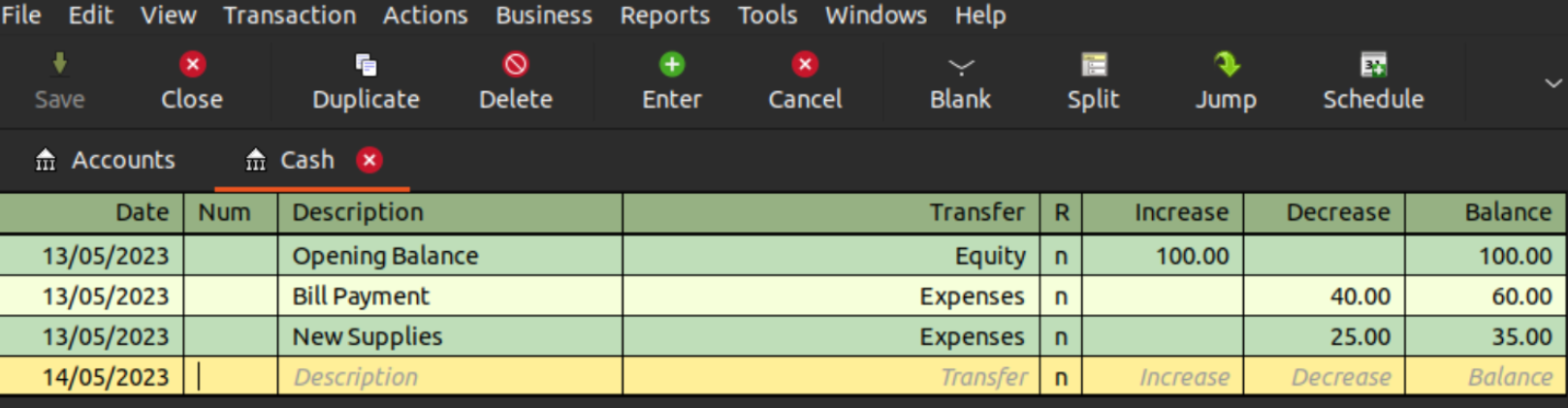

For example, let us have an opening balance of $100, and a subsequent bill payment of $40 and new supplies payment of $25.

Because Cash is a Debit account, debit (LHS) is an increase and credit (RHS) is a decrease:

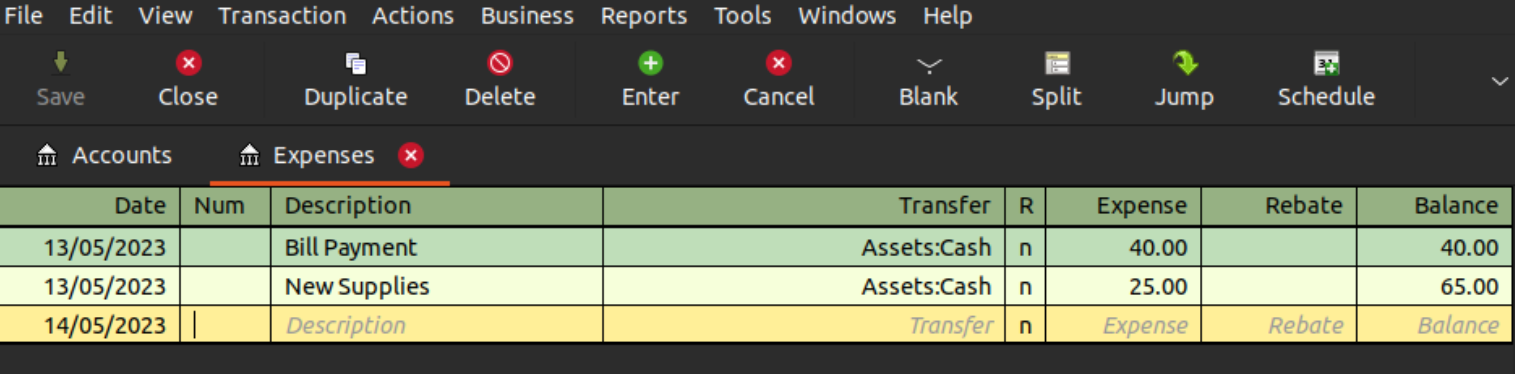

Similarly, Expense is also a Debit account. So debit is an increase and credit is a decrease:

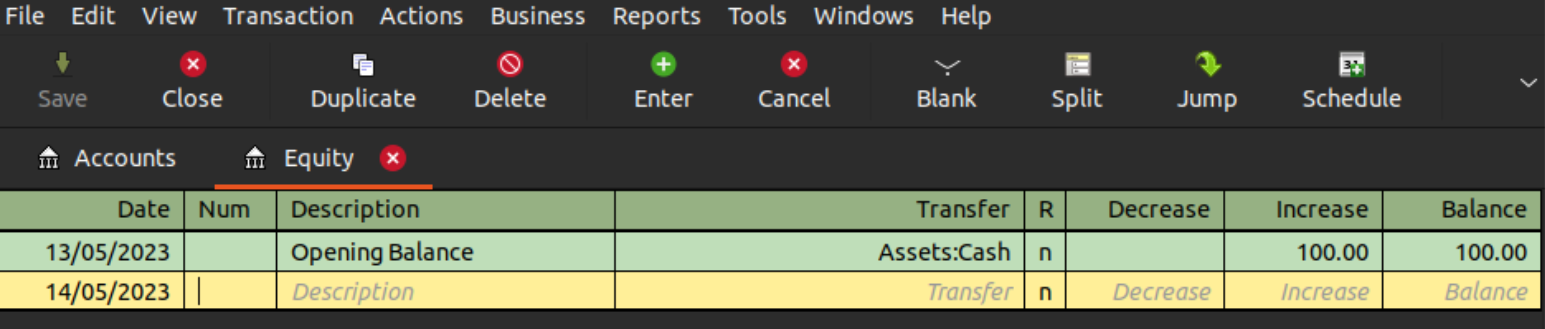

However, Equity is a Credit account, hence debit is a decrease and credit is an increase:

Overall:

Double-Entry Bookkeeping

In the above “T Accounts” section, you would notice that each transaction in the ledger involves another opposite entry in another account. This ensures the accounting equation is preserved.

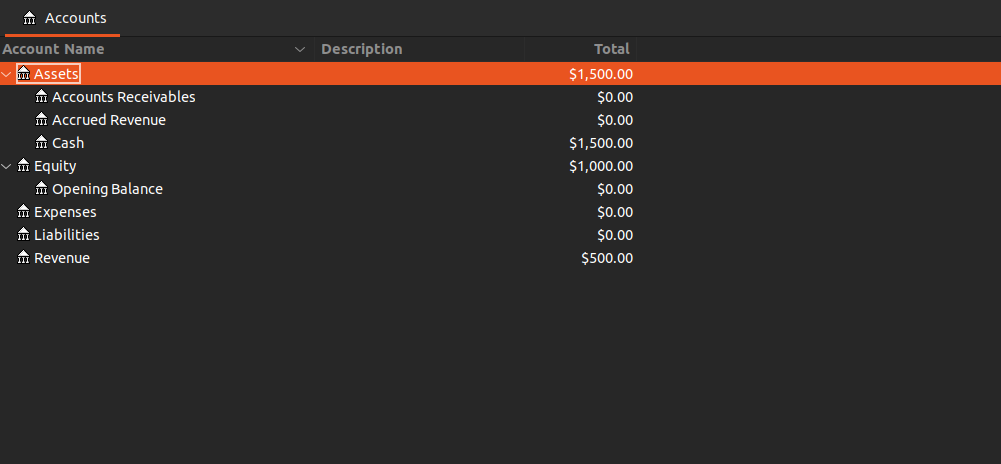

Let us do a more comprehensive example to showcase double-entry accounting. We have a new window cleaning business and the following transactions:

- The owner invests $100 in the business and got $100 in stock

- Business takes out a loan of $200 to fund its business

- Spends $30 in window cleaning equipments

- Spends $50 on cleaning supplies. Payment is made on account (in credit)

- Makes $150 in revenue and used half of cleaning supplies

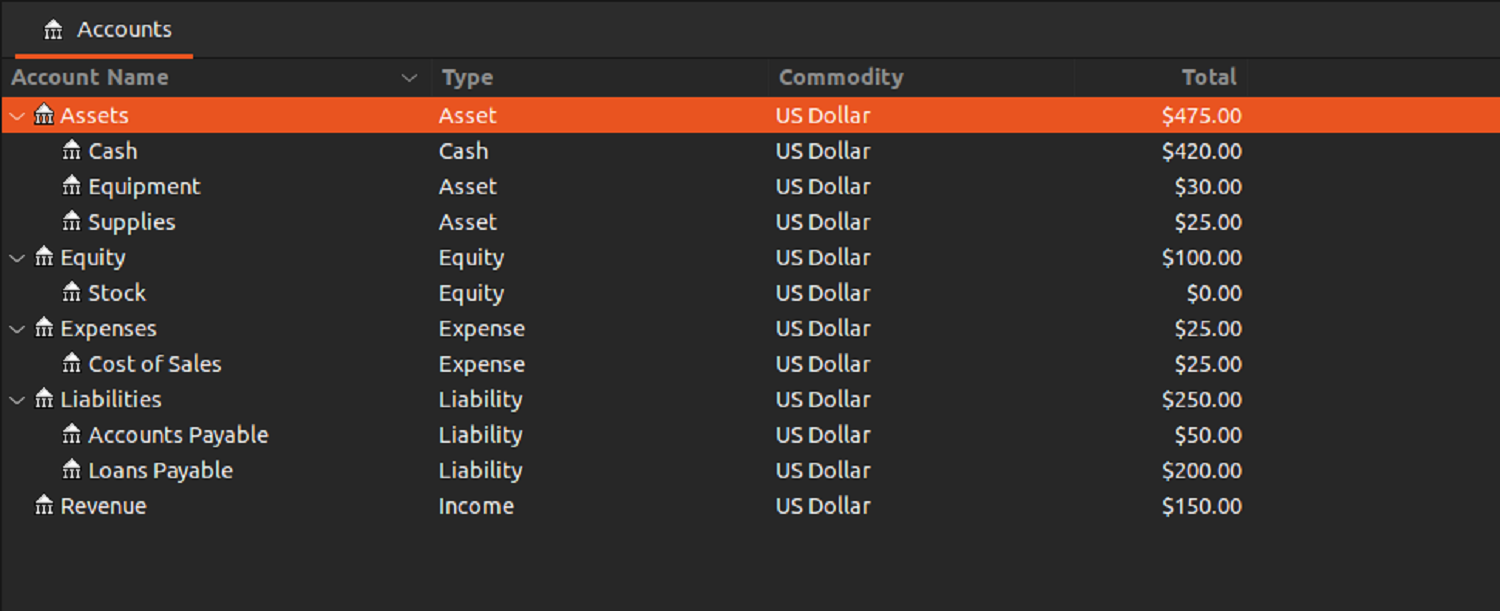

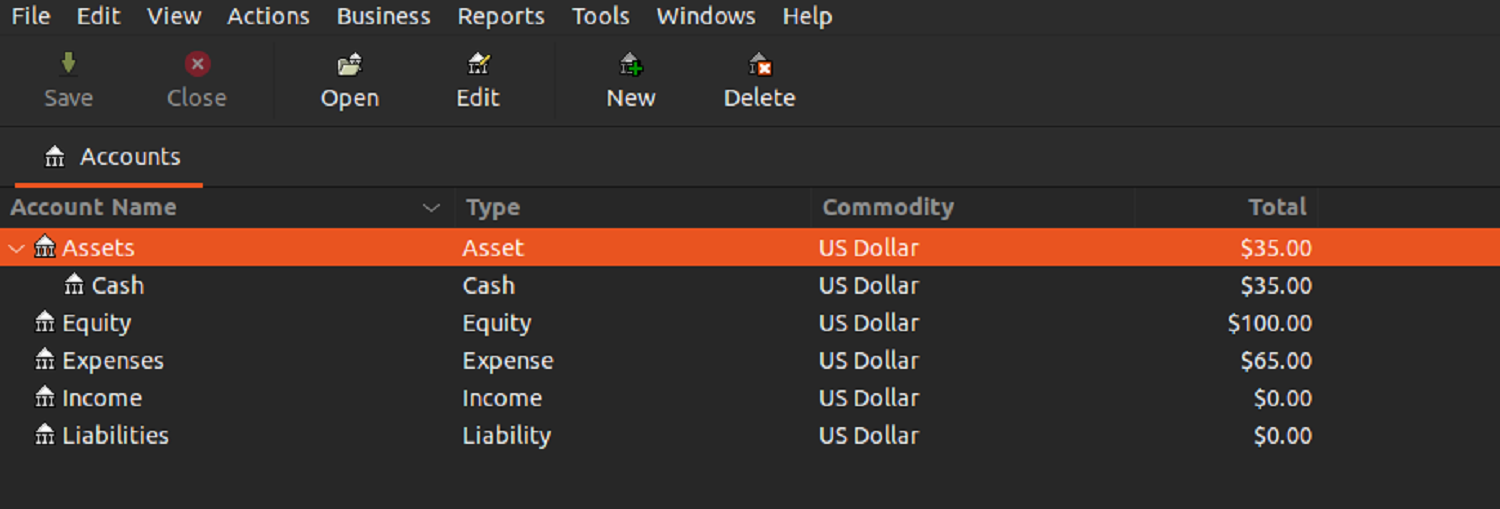

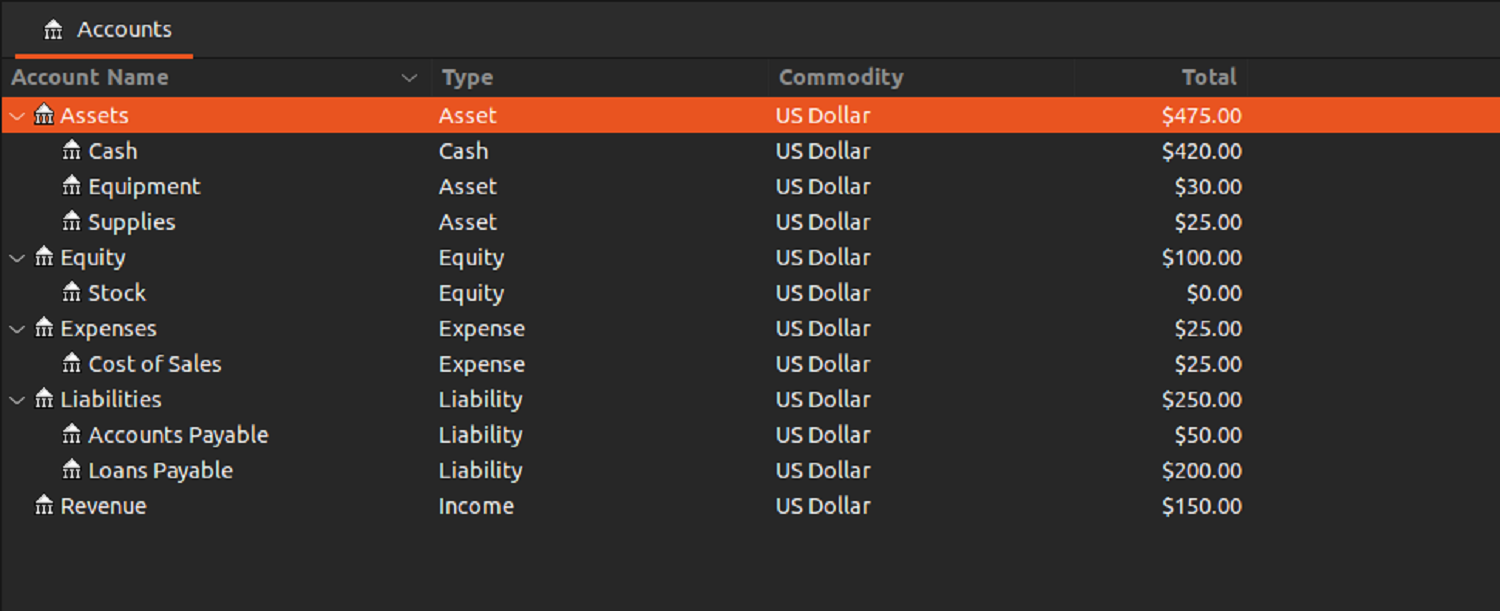

Let us input the transaction in GNUCash. First we look at the final accounts after inputting all transactions:

And each accounts separately.

Asset accounts:

Liabilities accounts:

Revenue accounts:

Expense accounts:

Equity accounts:

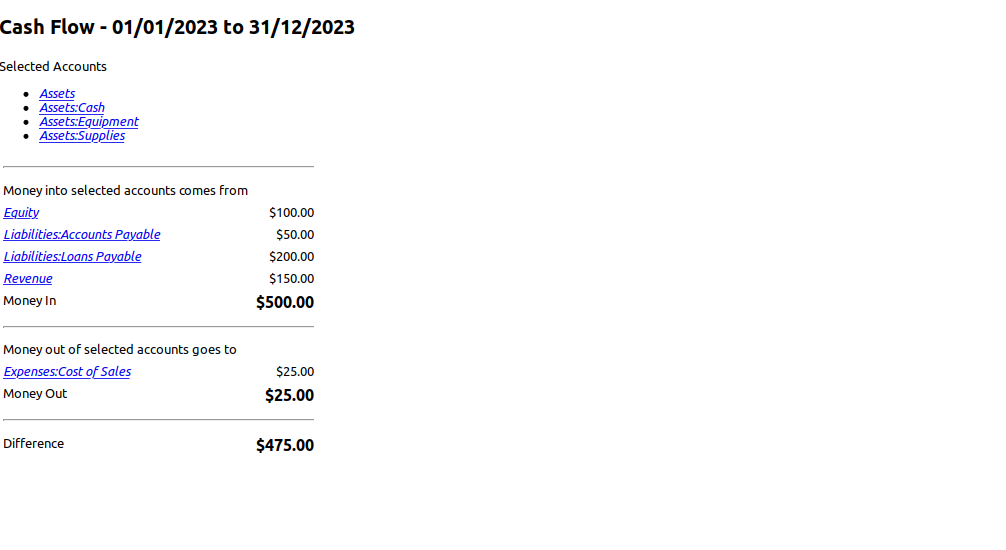

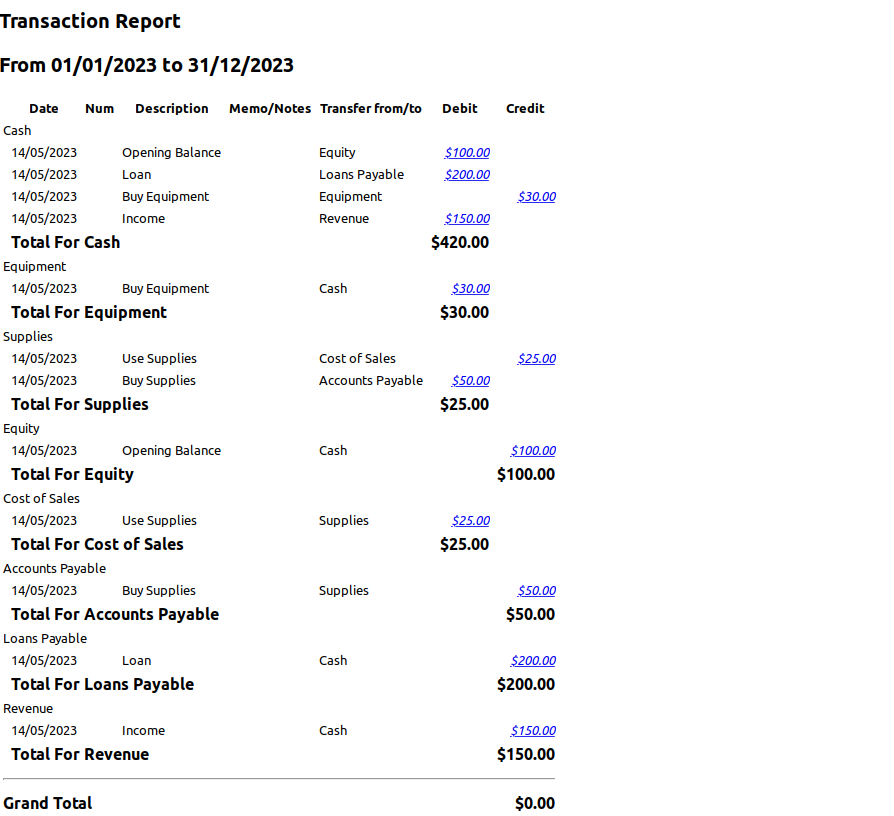

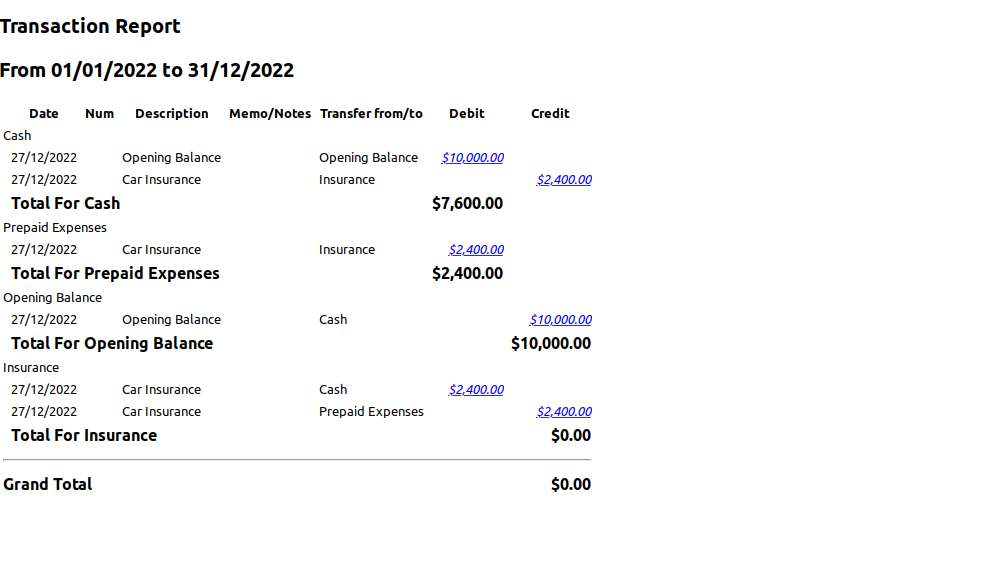

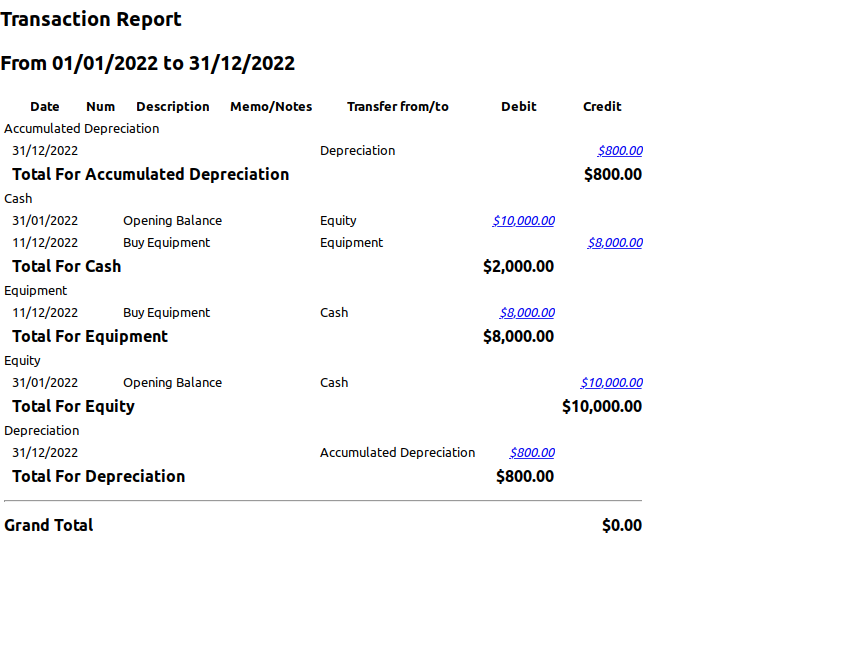

In GNUCash, we can run the cash and transaction report:

Cash Report

Transaction Report

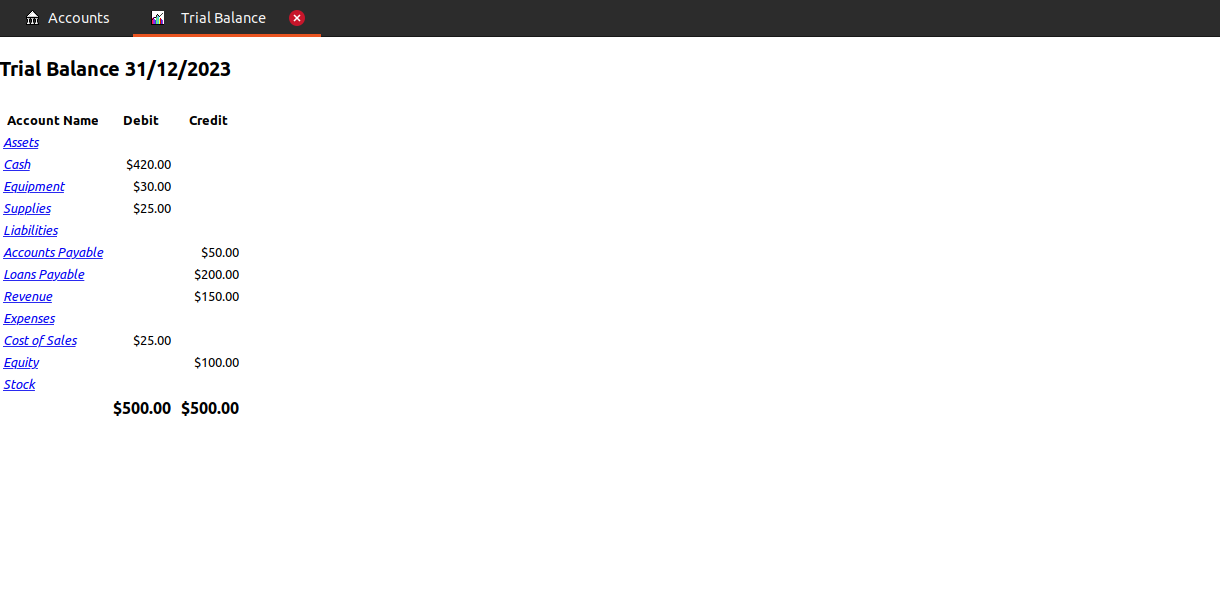

Trial Balance

Trial Balance is an internal report that is typically run at the end of day to show the closing balances of all accounts and to check for errors. Only nonzero balancse are ordered with assets, liabilities, equity, revenues and expenses:

Adjusting Entries

Adjusting entries are journal entries that we post at the end of each accounting period in order for the books to be in alignment with the accrual method of accounting.

Picture 1) a seller providing goods or services, the 2) seller handing the buyer an invoice and 3) buyer handing the seller cash. If the 3 parts span multiple accounting periods, we are going to get adjusting entries. This is due to the accrual basis of accounting where revenue is recognized as it is earned, and expenses are recorded as it is incurred.

In short, we will first hold the revenue/expense in the balance sheet in the previous accounting period and release them to the income statement in the next accounitng period.

There are two broad categories of adjusting entries:

- Prepayments

- Accruals

Prepayments

Goods/Services are deferred to the future and cash is paid in the previous accounting period. Prepaid Expenses are from the buyer side and Deferred Revenue are on the seller side. These balance sheets entries are released to the income statements as goods/services are delivered.

Prepaid Expenses

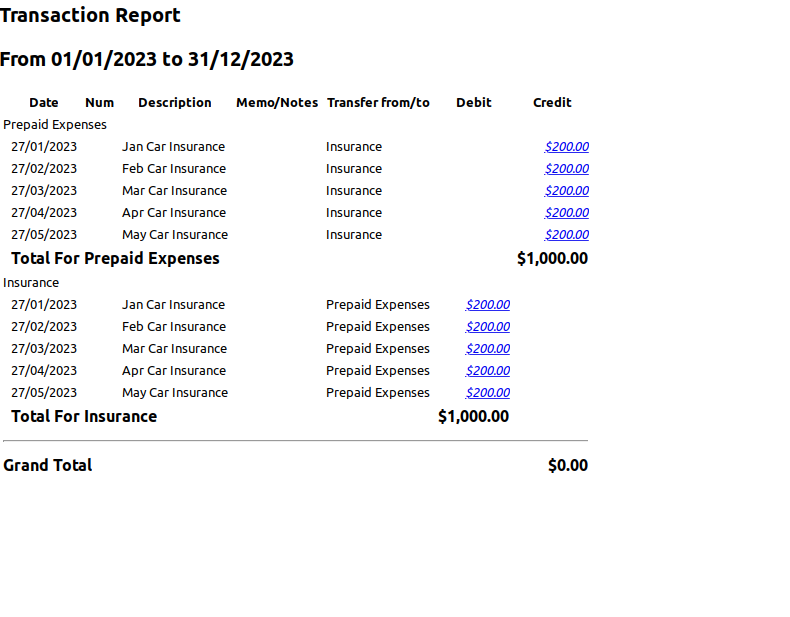

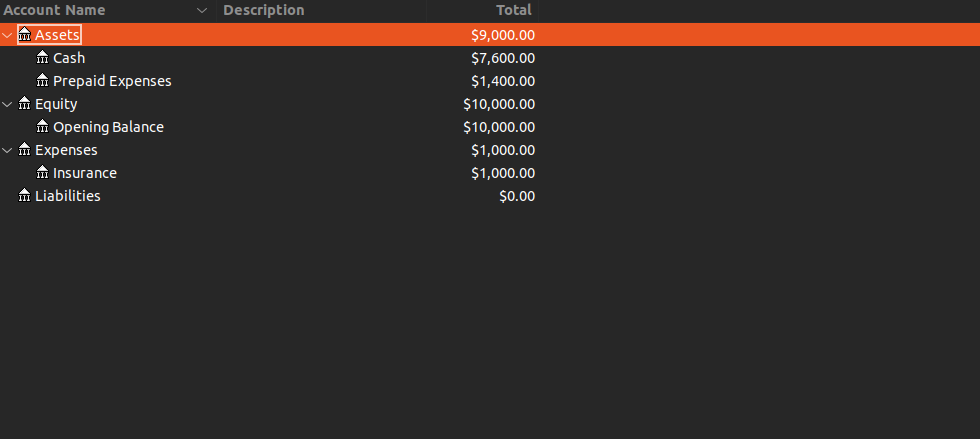

Prepaid expense is a future expense that has been paid in advance. For example if you buy a $2,400 car insurance in advance in Dec 2022 for the year 2023. In the 2022 accounts, you expense the payment. Assuming we have $10k for the opening balance.

Come 2013, we are going to need to add some monthly adjusting journal entries. We need to recognize \(\frac{1}{12} \times \text{2,400}\) each month. At the end of May:

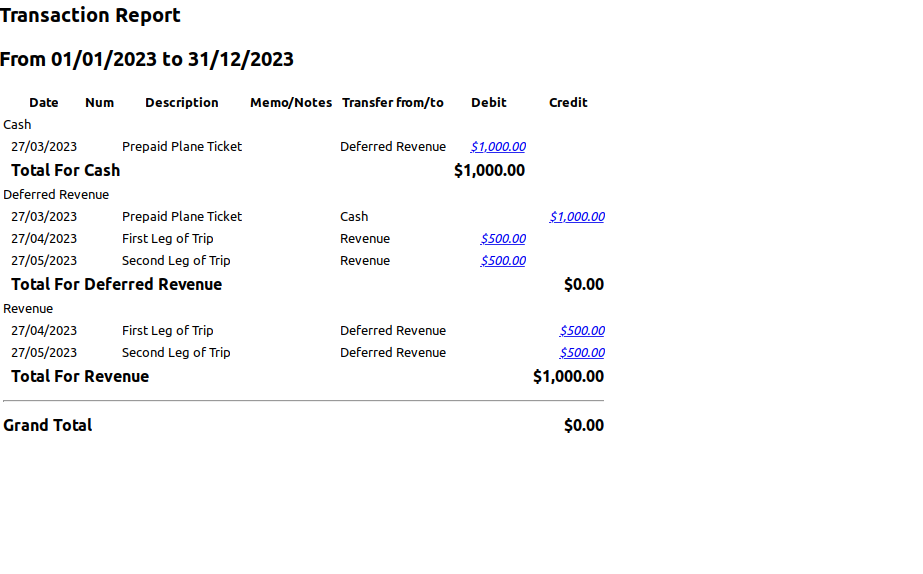

Deferred Revenue

The payments that a business receives in advance for goods/servies that haven’t been delivered or provided.

In this example, imagine you are a pilot that receive payment of $1k in Mar 2023 for a round trip. The first leg of the trip is provided in Apr 2023 and the returned leg is provided in May 2023:

Accruals

Goods/Services happened in the past accounting period but payment is done in the next accounting period. Accrued Expenses is from the buyer side and Accrued Revenue is on the seller side. These balance sheets entries are released to the income statements as cash are paid.

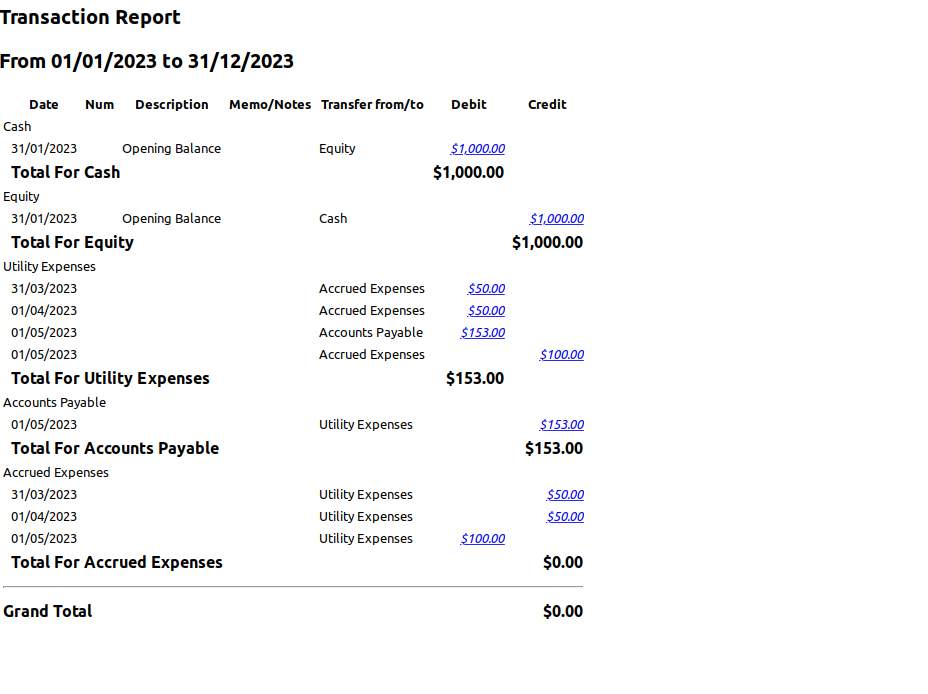

Accrued Expenses

A past expense that hasn’t been recorded or paid for yet. A good example is utility bill. We will first consume water and electricity before paying for it.

Suppose we incurred two months of utility bills, estimated $50 per month for the month of Feb and Mar. We got the bill in Apr and the bill came up to $253 but did not pay in cash yet. So we would document it in Accounts Payable. The accounts would look like this in Apr:

Accrued Revenue

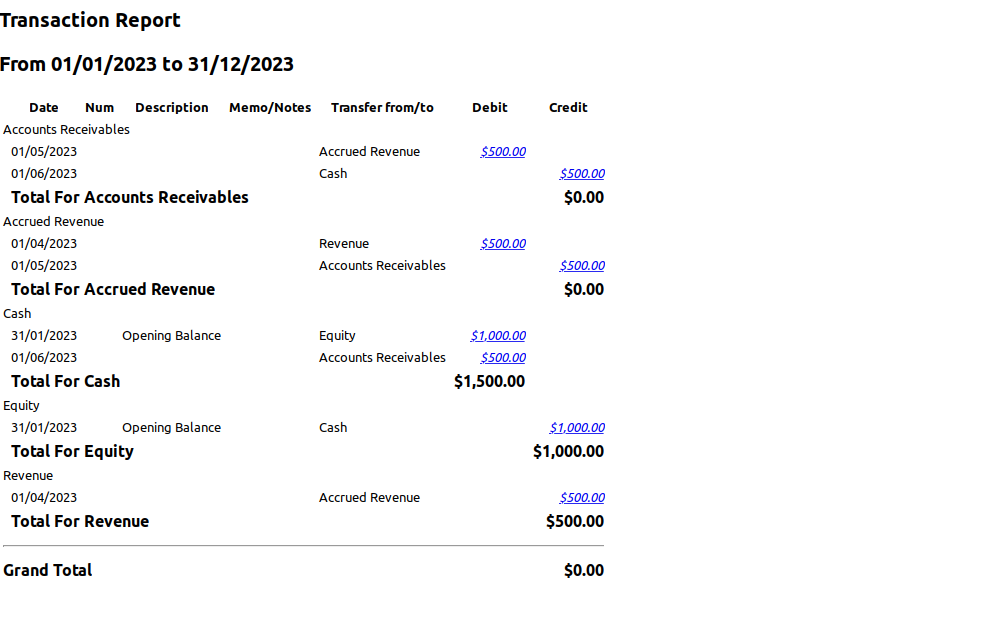

Accrued revenue is revenue that has been earned but not invoiced yet.

For this example, you are a website developer that has done the work for $500 in Apr but not being paid yet. The invoice was sent out in May and paid in cash in Jun. The following accounts will be affected:

Depreciation

Depreciation is the process of reducing the book value of a tangible fixed asset due to:

- Use

- Wear and Tear

- Passage of Time

- Obsolescence

There are a few ways of accounting for depreciation:

- Straight Line Depreciation

- Double Declining Balance

- Units of Production Method

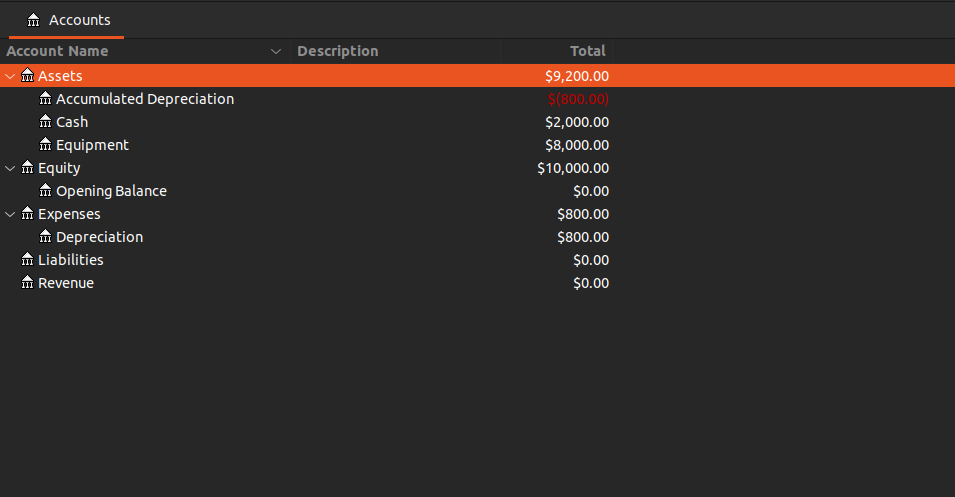

For demonstration, we will do a simple straight line depreciation. Assuming we bought an equipment for $8k, and depreciate it $800 every year.

Accumulated Depreciation account is what as known as Contra Asset account. To get the book value of the equipment, just net the Equipment account with Accumulated Depreciation account.

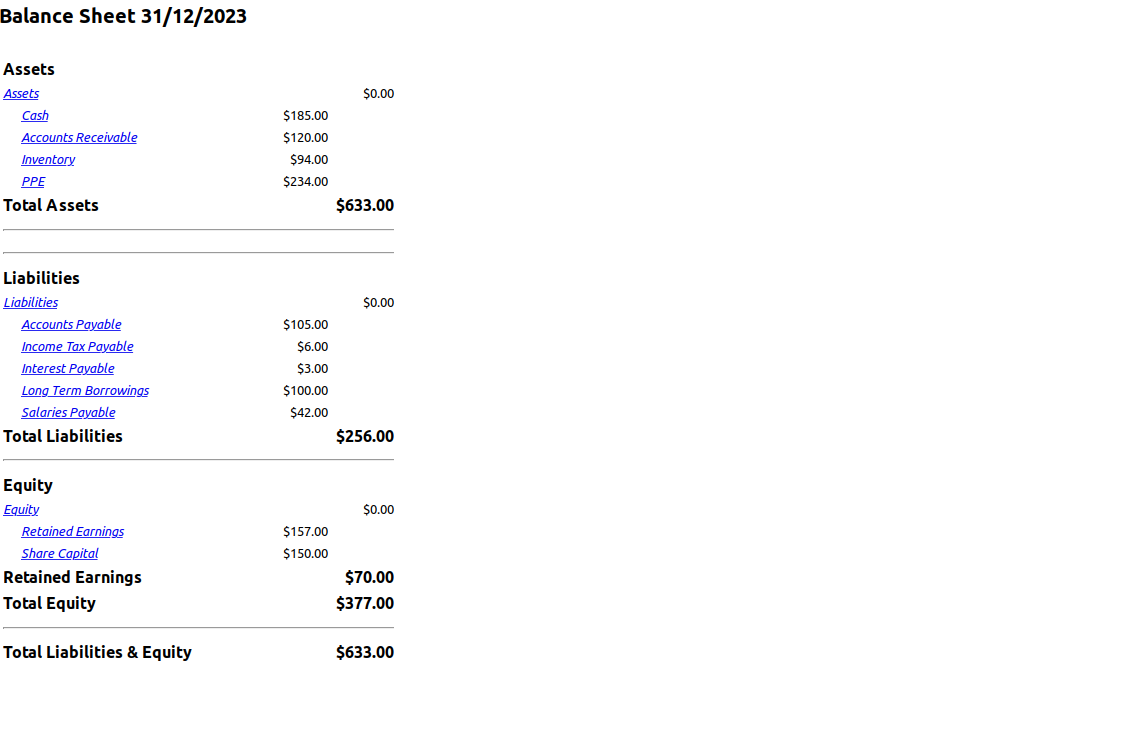

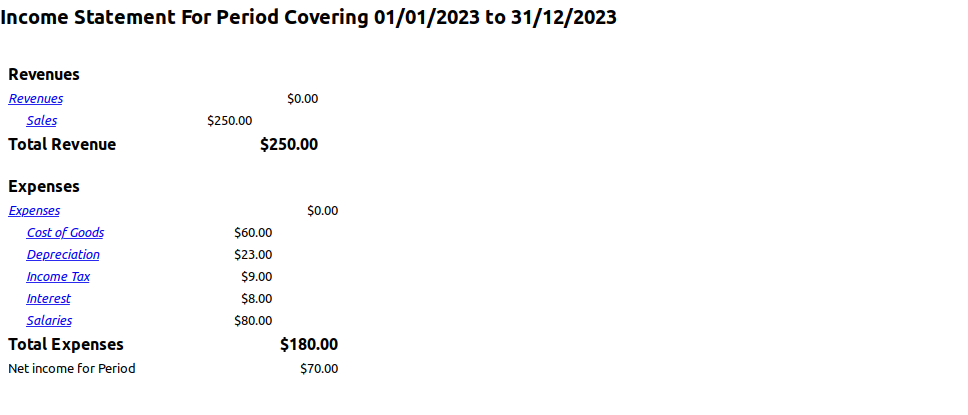

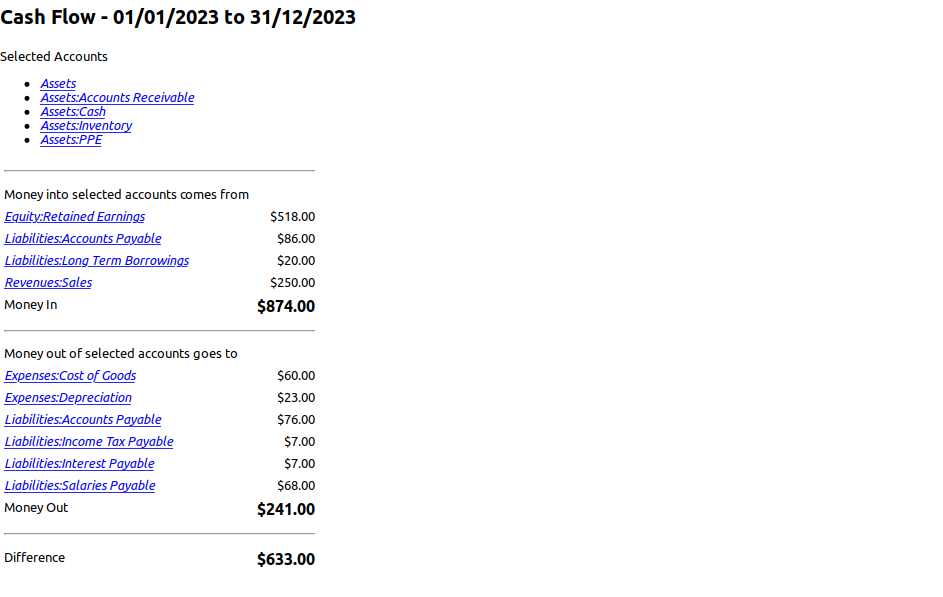

CashFlow Statement

A cashflow statement is a summary of a business’s cash inflows and outflows over a period of time. Essentially a cashflow statement is what you get when accounting under the cash method rather than accrual method.

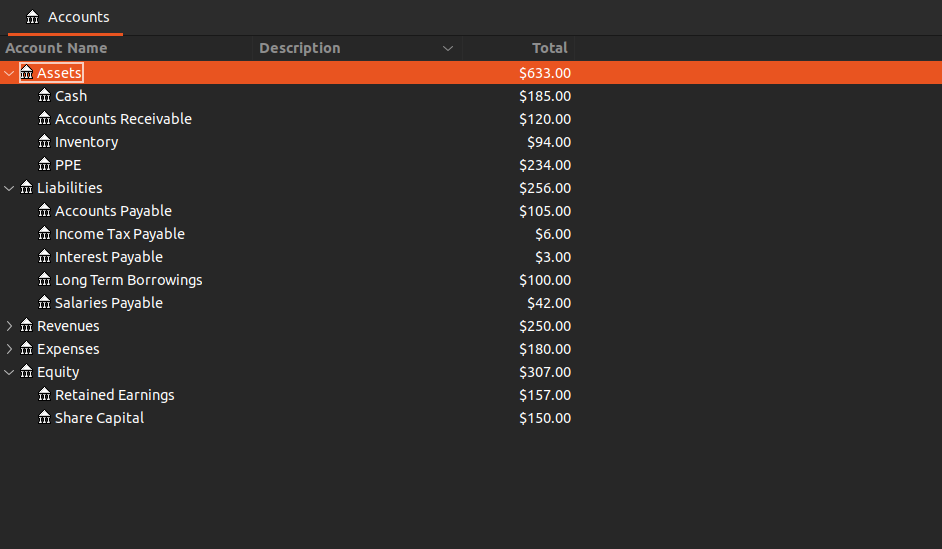

Taking the example of the video and generating the balance sheet, income statement and cashflow statement:

We will recreate a more conventional direct method for cashflow statement here for comparison:

Direct Method

| CashFlow Receipts From Customers | 228 |

| Cash Paid to Suppliers | (76) |

| Cash Paid to Employees | (68) |

| Interest Paid | (7) |

| Income Taxes Paid | (7) |

| Net CashFlow From Operating Activities | 70 |

| Purchase of PPE | (70) |

| Cash Receipts From Sale of PPE | 15 |

| Net CashFlow From Investing Activities | (55) |

| Proceeds From Long Term Borrowings | 20 |

| Net CashFlow From Financing Activities | 20 |

And similarly for the indirect method (note the difference is only for operating activities):

Indirect Method

| Net Profit | 70 |

| Add Back Non-Cash Expenses | |

| Depreciation | 23 |

| Amortization | 0 |

| Gain on Sale of NCA’s | 0 |

| Adjust For Movement in Working Capital | |

| Increase in Inventory | (26) |

| Increase in Receivables | (22) |

| Decrease in Payables | 25 |

| Net CashFlow From Operating Activities | 70 |